It is so hard for people to get out of the notion that life is a zero-sum game. They think that if one man benefits, another must lose. But in a free market, both people can benefit.

—Milton Friedman1

After dominating the world since the beginning of the twentieth century, and with particular force in the immediate post–World War II period, the American economy has, since the late 1970s, allowed its productive dominance to wither. Iconic U.S.-based corporations ceded market share to (mostly) Asian competitors, often opting not to fight back and instead outsourcing and offshoring their own production to factories in lower-wage places.

Restoring large-scale, competent manufacturing in the United States will require a thoroughly new and uncharacteristically comprehensive economic policy. Such a policy will need massive government support, enforcement of significant new rules (the stick to the carrot of state support), and—perhaps paradoxically—the reversal of five decades of attacks on workers and their unions.

Indeed, as we will show, the new policy will have to put the worker front and center in the firm. Workers’ expanded role will be born of, and maintain, a higher level of labor-management conflict than the United States has seen since the early 1940s. Although it may be surprising to most readers, that’s actually a very good thing, so long as that conflict is about effort and reward in the context of higher productivity—which we’ll refer to as productivity bargaining. We will argue that, while national pattern bargaining (the standard approach of most U.S. unions) today) is effective at setting baseline compensation, it misses the bigger picture of productivity and, therefore, costs. Productivity bargaining, by contrast, is focused on local production and plant performance to identify input factors whose underutilization adds avoidable costs and reduces output. Our approach links shop-floor conflict to productivity growth.

The fundamental question is: can a revitalized union movement spur measurable improvements in American industrial productivity and, if so, how? What would workers, unions, companies, and policymakers need to do differently? And at what scale?

The Biden Break

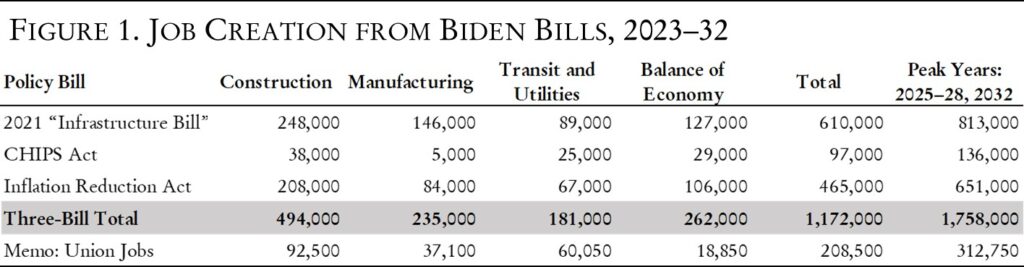

These questions are new in the American context. Before 2021, the idea of using government policy to encourage reindustrialization had not been seriously considered for decades. Given cover by the need for bold stimulus to counter the Covid-19 pandemic, under President Joe Biden the federal government has advanced and funded several large-scale efforts to stimulate manufacturing investment in the United States, with particular emphasis on physical infrastructure, vehicle electrification and grid modernization, renewable energy, and computer chip fabrication. The effort is comprised of three bills that were signed into law between November 2021 and August 2022. All three cover the period from 2023 to 2032. While each bill targets different sectors, for our purposes they can be considered as a single initiative comprising the investment ledger of “Bidenomics.” They are the Infrastructure Investment and Jobs Act (IIJA), the chips and Science Act (chips), and the Inflation Reduction Act (IRA). (Although nearly two-thirds of projected IRA spending is slated to occur in red states, not a single Republican voted for the IRA. The Infrastructure and chips Acts fared better with GOP lawmakers, no doubt thanks to their “catch up to China” flavor.)

There can be little doubt that the scale of this three-pronged initiative is unprecedented in postwar U.S. history. Over the past century, only during the periods 1934–38 and 1942–45 did the United States spend even one full percentage point of GDP on these kinds of physical investments. Under the Biden bills, hard public and private investments would slightly exceed 1.3 percent of U.S. GDP and, in peak years, reach 1.7 percent, tying the peacetime record set in the New Deal’s core five-year period, 1934–38. As impressive as those numbers sound, even in the peak years they don’t equal China’s public investment in industrial support: according to analysis by the Center for Strategic and International Studies, in 2017–19, just the public portion of China’s investments in industry exceeded 1.7 percent of GDP.2 And they pale in comparison to, say, the Marshall Plan, whose 1945–49 resources made up 3 percent of GDP in both France and Germany.

The Biden investments both address new challenges—such as curbing utility and transportation sector emissions of greenhouse gases—and aim to rectify more than four decades of insufficient maintenance of existing infrastructure. For example, of the nation’s 620,000 bridges, nearly half are more than fifty years old and forty-five thousand of them have been deemed “structurally deficient.”3 Two-thirds of those forty-five thousand are due for replacement or upgrades under the bills.

The full impact on American industry of the Bidenomics investments is difficult to project, however, because it is hard to know exactly how much private investment they will leverage. The recent slowdown in the growth rate of electric vehicle (EV) sales and the resulting pullback in battery and other EV-related investment plans illustrate one of the difficulties: in the two years since the IRA was signed into law, private companies announced $240 billion in clean energy investments, but in the past several months, they’ve delayed or backtracked on about one-third of those “commitments.”4 That said, the data available so far point to significant leverage: inflation-adjusted public plus private spending on manufacturing and industrial construction set a record in 2023, surpassing the previous one set way back in 1964.

Relying mainly on Congressional Budget Office (CBO) numbers to deflate White House press release figures, stirring in useful projections from the Office of Management and Budget (OMB), and assuming that 15 percent of the spending is eaten up by administrative costs and other rentier losses, we can infer that the three laws will likely fund or catalyze roughly $2.3 trillion in nonresidential investment over ten years, a plurality of that in the utility sector, where federal spending and regulatory suasion work in tandem.5 This matters because, even if a subsequent U.S. administration were to rescind or defang the regulatory sticks, it would likely leave the laws’ carrots in place. Also making it less likely that subsidies will be withdrawn is the appetite for them in red states.

As for the job creation associated with the Bidenomics investments, detailed projections not issued by the White House itself are hard to find. Usefully, CBO and the Congressional Research Service (CRS) have both analyzed some or all of the bills; the CRS helpfully put the impacts of the chips Act, in particular, in the context of trading partners’ semiconductor policies. Both Moody’s and the Brookings Institution have produced reputable meta-analyses, comparing and contrasting the projections from a number of data sources.6 Using widely accepted estimates of the number of construction and manufacturing jobs associated with each dollar of investment,7 we can back into reasonable forecasts of the employment impact of Bidenomics’ direct and induced investments. Once we do that, we can see whether the policy meaningfully moves the needle in terms of making American industry bigger.

During the first two to four years that the three-bill policy is in effect, the majority of jobs created each year—roughly 1.5 million—will be in construction, but a good deal of what’s being constructed will have to be manufactured: steel and cement for tens of thousands of miles of road repairs, for repair or replacement of ten thousand bridges, for new solar cell and chip fabrication factories, and for all of the parts that will be needed to build the twenty-four thousand buses, five thousand rail cars, and thousands of miles of track and signals slated in the bills. In the middle years of the ten-year implementation period, most of the jobs will be in manufacturing. In the last two years (2031–32), construction’s share of the jobs will grow again, as projects must be launched before federal funding sunsets. Our best guesses, informed heavily by the Moody’s and Brookings studies, are that what Americans think of as “industry”—manufacturing, maintenance, electricity generation and storage, and the construction of the facilities in which they are performed—will add just shy of 1.2 million jobs a year, about 20 percent of them union jobs.

In addition to direct federal investment and the private spending it induces, the three Bidenomics bills include substantial tax incentives for employers who pay prevailing wages and employ registered apprentices on qualifying projects.8 Construction (11 percent), manufacturing (about 8 percent) and utilities (just under 20 percent) are more unionized than the private economy as a whole (6 percent). The pay scale and apprenticeship rules and incentives in the three bills will also probably result in unionized firms’ taking a significantly larger share of the business driven by these policies.9 Even though the union pay premium has declined as union density has dropped, on average an American worker with a forty‑year career in a union firm earns $1.3 million more over his or her lifetime than an average nonunion worker.10

Two sobering baselines must be set, however. First, the organized proportion of the U.S. workforce is vanishingly small. In 2023, union contracts covered just one in ten of all American workers, and in the private sector just one in sixteen. The high level of public support for unions and their demands owes, arguably, less to some newfound appreciation for collective bargaining among the working class than to the widespread disgust—arguably brought into public view by the impunity and gluttony of financiers and their government enablers during the Great Recession—at the level of U.S. income and wealth inequality.11 In both 1947 and 1978, American workers got about two‑thirds of GDP as income from their labors. “Now, they’re getting . . . just a little bit over half.”12

Deindustrialization and the Decline of the

U.S. Auto Industry

But is Bidenomics’ support for organized labor consistent with its industrial policy goals? To even begin to consider labor’s possible role in helping to reindustrialize the U.S. economy, one must face up to how the United States got so deindustrialized in the first place.

The consensus story is well known: Asia’s mercantilist juggernauts built wealth through lower-cost manufactured exports, while American corporations relocated their production to lower-wage nations in response. In industry after industry, U.S.-based corporations reacted to Asian competition in a surprisingly similar matter: exiting the low end of each market (commodity textiles and steels, small cars, low-end appliances, and computer chips), offshoring and outsourcing to reduce the draw on their own capital, closing their own plants, and seeking concessions from their remaining unionized employees.

In semiconductors, U.S. production as a share of global output dropped from 60 percent in 1980 to 37 percent in 1990 to 10 percent in 2023.13 In steel, U.S. production and employment both dropped by half between 1974 and 1984; by 2020, China was producing five-ninths of the world’s steel, the United States just one-sixteenth.14 In automotive manufacturing, the trio of (formerly) Detroit-based automakers had a domestic market share of 84 percent in 1978; that dropped to 64 percent by 2000 and to 43 percent last year. Given our own backgrounds in the auto industry—one working at General Motors and the other at the UAW’s headquarters—we will focus our analysis of deindustrialization, and possible reindustrialization, on that sector.

Deindustrialization was a national disaster that resulted from two types of unforced errors—mistakes which must be understood and addressed if the United States is to reindustrialize. The first was a fundamental misunderstanding of the economics of manufacturing firms by their management, by neoclassical economists, and by human resources specialists. As U.S.-based automakers (and, before them, steel, textile, and apparel makers) lost market share to lower-cost Japanese companies, American managers and economists drew two incorrect conclusions. The first was that the Japanese advantage was rooted in lower vertical integration, which was a misreading of Japan’s keiretsu arrangements, in which automakers held equity in and backstopped investments by their suppliers. The second was that Japanese labor relations were more “cooperative” and less adversarial. While it is true that Japan’s militant, Communist-led unions were broken (with American help) in the 1950s, this too was a fundamental misreading: the “labor peace” that Japan-besotted academics thought they were seeing was, in fact, based on a system in which factories were run by a highly engaged workforce overseen by surprisingly few managers. We will return to this point later.

A second critical error was Wall Street’s punishment of those American manufacturers with the temerity to reinvest earnings in their own growth and process improvement. Led by Drexel Burnham Lambert, a generation of “corporate raiders” laid waste to scores of iconic companies, demanding that they instead return earnings to shareholders. In the 1980s, Drexel and subsequently others threatened, and in some cases took over, companies using infamous “greenmail” and “highly confident letter” tactics, and in the process drove the dismantling of targeted companies’ vertical integration, so as to “free up” their capital. In a context of burgeoning investment by Asian industrialists and governments, this was a recipe for disaster. U.S.-based companies were hollowed out just as competitors in Japan, then Korea, and finally China forwent short-term profits in pursuit of market share gains and future technological dominance.

The automotive story of the 1980s makes clear just how wrong-headed these imagined solutions were. Until the U.S.-based automakers began to bleed market share in small cars in the 1970s—first to Volkswagen and Renault, and later to Toyota, Nissan, and Honda—they (and especially GM) maintained high levels of vertical integration. These companies invested enough capital (equipment and tools) to ensure that the productivity of their (mostly UAW) workforce would easily offset their higher pay relative to nonunion workers. In 1978, two in every three workers in the motor vehicle and parts industry worked at GM, Ford, or Chrysler; only 336,000 worked at supplier-owned plants, and 195,000 of those toiled at UAW-organized supplier facilities. Only 141,000, or 13.7 percent, of the workers in the sector were not in unions. The so-called Detroit Three automakers built 83.6 percent of all cars and light trucks sold in the United States.

Two decades later, the Detroit Three’s share was down to 68.2 percent. Of the 1.276 million men and women working in the automotive and automotive parts sector (which was 250,000 more than in 1978), 913,000 (or 71.6 percent) were working in nonunion plants, roughly 200,000 at the U.S. factories of Europe- and Asia-based automakers, and more than 700,000 at nonunion supplier plants, a five-fold increase from twenty years prior.

As Department of Labor economist Stephen Herzenberg noted in his seminal 1991 study, sharply declining Detroit Three employment due to outsourcing to nonunion plants had unexpected results. Most nonunion suppliers, pressured by oligopolistic price cutting by their customers, faced substantially higher costs of capital than the largely self‑financed automakers, which could also access highly liquid public capital markets; as a result, those suppliers had sharply lower productivity.15 For their part, the Detroit Three automakers lost control of production costs and component quality. (That lower productivity was no doubt a large part of why industry employment grew by nearly a quarter, though 1998–2001 were also strong new-vehicle sales years.) Thus, outsourcing most parts-making didn’t result in measurably higher Detroit Three profits; those only came a decade later, courtesy of the dumb luck of a huge swing from cars to pickups and SUVs (which cost about $4,000 per unit more to build but sell for an average of $11,000 more). Ironically, because the UAW contract required the self-shrinking automakers to slough off workers in seniority order, the most experienced—and thus highest-paid and most skilled union workers—survived the layoffs. Had the Detroit Three been able to cast off their most expensive workers, the results of their downsizing would have been far worse.

Moving work from high-wage, high-productivity facilities to lower-wage, lower-productivity facilities was the result of the new Detroit Three strategy encouraged by Wall Street’s Drexel school and abetted by academics. In theory, the Detroit Three, by following this strategy, could have freed up capital to design and build competitive new models, to optimize their facilities to eliminate cost-sapping bottlenecks, and to invest in upgrading their workers’ technical knowledge and capacity to operate plants with less supervision. But, in reality, they did not. If anything, these automakers became less competitive while their market share continued to decline.

The EV Challenge

In a tragic new unforced error, the Detroit Three automakers are botching their most important current challenge—the migration of the new-vehicle fleet to battery electric power. Although electric vehicles (EVs) have become a partisan flashpoint, even the least woke automotive and oil-and-gas executives grasp that the future will involve more electric. This fact is rooted not only in climate change concerns or in the markedly superior performance of EVs vis-à-vis gas- and diesel-powered vehicles on a number of metrics, but also in the fact that the U.S. fossil fuel industry’s dominant customers include not only car and truck drivers but also electric utilities, which depend on natural gas for half of their generating capacity.16

China’s government, which in the next five years will boast a new-vehicle market as large as those of the United States and the EU combined, has made a decision to drive toward an all-EV future. Thanks to its state having successfully catalyzed the emergence of a set of low-cost, high-volume producers of the critical technologies underpinning electrification—batteries, electric vehicles, and solar photovoltaic cells—China’s path will almost certainly become the world’s.17 European and (for now) American emissions standards favor lower-emission vehicles, and recent breathless “news” about a stall in EV sales growth has not altered long-term forecasts.18

Europe and the United States may make token moves to decouple from China’s economy in batteries, EVs, and other areas, but the die is cast. A period of higher tariffs to insulate supposedly emerging “infant industries” will surely give way to a blend of Asian imports, including via free-trade-partner Mexico and new Chinese company plants in North America. (This will recapitulate what happened in small cars in the 1980s and 1990s: offshore automakers used North American plants to get around “voluntary restraints” and the so-called chicken tax on pickup trucks.)

This era of Chinese battery and EV dominance does not come without its agonies. The U.S.- and Europe-based automakers may talk a good game on EVs and will bring a growing number of electric models to their home markets, but the fact is that people who are paid to look at the automotive markets know what’s what. “We believe that Western auto firms (including Tesla) have come to a unanimous and simultaneous realization: China has won the contest for EV supremacy,” writes Morgan Stanley auto analyst Adam Jonas in a May note to clients. “From this point, the industry is likely to enter a new phase of capex spend (lower), protectionism (higher) and cooperation with China (eventual).”19 Bank of America analyst John Murphy went even further, saying a month later that “I think you have to see the [Detroit Three] exit China as soon as they possibly can” so they can conserve capital and face up to the “harsh cost-cutting measures they would have to take to be competitive with EV manufacturers like Tesla [and] . . . carmakers abroad.”20 We suspect that Bank of America, Morgan Stanley, and their wealth management clients will see lower automaker capex as a good thing, as it foretells higher dividends and more share buybacks.

Jonas’s forecast of “eventual . . . cooperation with China” is an easy call. Despite additional subsidies, U.S.-based companies that have specialized in surrendering all but the most hyper-profitable vehicle segments are hardly likely to be sound stewards of new state largesse. In addition, it is a largesse offered with no apparent strings attached: automakers are free to fling their profits to shareholders while Uncle Sam foots the bill for battery and EV assembly complexes. For all the talk of “unfair” Chinese government subsidies to China-based EV makers, those subsidies went to serious companies with a laser focus on winning domestic and global market share; they were far more worried about displeasing their state benefactors than the owners of their shares. While these companies were, essentially, starting from scratch, the traditional American automakers were pursuing a quite different set of objectives, playing to “the markets,” just as Drexel, channeling Milton Friedman, would have wanted them to do.

For a brief moment in 2021, the Detroit Three saw a chance to try for a step-function increase in their stock market valuations. Casting themselves as tech companies, they acquired a handful of EV- and driverless-car-focused start-ups. They touted ambitious and capital-hungry plans to catch and eventually surpass Tesla in EVs. Soon enough, however—indeed, within a single calendar quarter—the blush was blown off the rose: none of the three were able to produce batteries at scale, despite joint ventures with supposedly proven Korea-based partners. EV production targets were routinely missed, and lower volumes meant higher unit costs; as if by habit, the automakers raised their prices to limit the losses. (Only slightly better launches were achieved by VW, Mercedes, and BMW in Europe and China.)

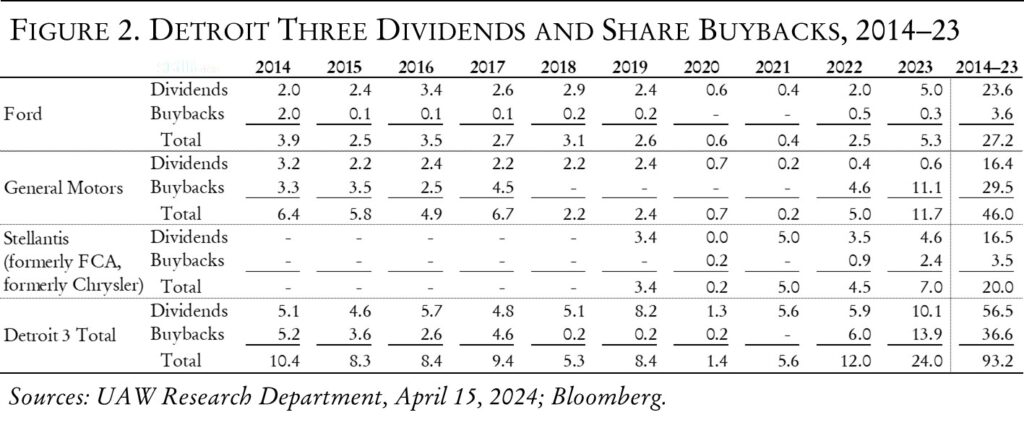

Then, with consumer demand for EVs stalling in the first quarter of this year, the automakers—as Jonas explained—shifted gears and suddenly assured the markets that they were prudent stewards of their scarce capital, especially after agreeing to expensive new contracts with the UAW. Capex for EVs would be throttled back, the focus on high-margin gasoline-powered trucks sharpened even further, and shareholders put ahead of investments in the future. So far in 2024, GM has bought back an additional $6 billion of its shares, raising its ten-year total to a cool $52 billion. These dividend and buyback payments—totaling just shy of $100 billion over the past decade—dwarf Chinese subsidies to its battery and EV producers.

China’s success also lays bare the bankruptcy of the Drexel school’s drive to divest from parts-making and to reduce vertical integration in order to conserve capital. The three most successful homegrown Chinese automakers are all highly vertically integrated. The leader among them, BYD (in which Warren Buffett’s Berkshire Hathaway has long held a position), has caught up to Tesla globally in sales. Unlike Tesla and the Detroit Three, BYD is at least as self-supplying and vertically integrated as GM was in the 1960s: it makes everything from battery cells to motors to frames and body panels. In batteries, it is not only self‑supplying; it achieves scale economies by selling its batteries to other manufacturers. Backstopped by a government that sticks to a long‑term strategy—willing to see some firms fail along the way without abandoning its larger goals—BYD and other Chinese manufacturers dared to invest heavily and to develop and maintain competency in every aspect of their industry: electrochemistry, automotive design, production, testing, marketing, and in BYD’s case even creating a fleet of ships to carry its cars to world markets.

In the United States, major companies instead retreated to what big-name Harvard business theorists called their “core competencies,” which in auto turned out to be few and far between once exposed by Tesla and now the global EV challenge.21 BYD sells well-regarded EVs for as little as $8,500, and is approaching a 1 percent market share (and 10 percent of EVs sold) in the EU in its first year selling there.22 (Not surprisingly, its success—and the fact that, unlike Tesla, it is not yet building its cars in most of the foreign markets into which it sells—has led to a spate of tariff hikes by the United States, Canada, and the EU.23) Nor is the China model’s success solely, or even mainly, about low labor costs: “In commercial innovation China is also overturning old assumptions,” according to the Economist. “The batteries and electric vehicles it exports are not just cheap, but state-of-the-art. Huawei, a Chinese telecoms firm brought low after most American firms were barred from dealing with it by 2020, is resurgent today and has weaned itself off many foreign suppliers. Although it earns a third of the revenue of Apple or Microsoft, it spends nearly as much as they do on R&D.”24

Peter Johnson, an industry analyst, reported this year that, “After selling more vehicles than Honda and Nissan in the second quarter of 2024, BYD became the world’s seventh-largest automaker . . . [selling] 980,000 vehicles. The company now has over 900,000 employees . . . [making it] one of the largest employers in China and [it] is the largest [among] the over 5,300 companies listed on China’s mainland stock exchange. . . . [It] is also the world’s largest automaker in terms of R&D staff, with over 110,000 such employees.”25 BYD’s size reflects its high degree of vertical integration and makes for a shocking contrast to GM’s total global headcount of 170,000, which is down from more than 850,000 in the late 1970s.

Toward a Union Resurgence?

Meanwhile, throughout this long history of decline, the auto companies stepped up their attacks on the remaining union members. They threatened to move work away from the plants where the most militant local unions represented employees and into those where locals were most cooperative or, when appropriate, to outside supplier facilities. This “whipsawing” of locals sapped morale and led to the wholesale electoral defeat of local union officials at the most cooperationist locals, many of whom had to be rescued by being brought onto the UAW’s national staff. By tolerating such whipsawing, the national union lost the respect and confidence of many rank-and-file workers. This set the stage for an insurgency in the national union that rebuked the cooperationist strategy and culminated in a militant strike against all of the Detroit Three last year.

The 2023 insurgency also reflected members’ reaction to unforgivable mistakes that the UAW leadership made in the 2007–19 period, partly in response to the onerous concessions mandated by the government in return for the $90 billion in loans that bailed out GM and paid for Fiat’s takeover of Chrysler in 2009. By 2014, GM had $30 billion in the bank, but none of it went to reimburse the workers who had “taken one for the team” by giving up $11 billion in pay and benefits. The Obama administration’s Presidential Task Force on the Auto Industry that guided the restructuring of GM and Fiat-Chrysler did not mandate any pay resets, nor (incomprehensibly) did UAW leaders demand them. Auto executives earned more and more, not just because their companies became more profitable but because their hand-picked boards approved dividend increases and stock buybacks that inflated the share prices to which CEO compensation was closely tied.

When the union agreed to an “in-progression” lower tier in 2007, it rightly insisted that lower-tier workers make up no more than 25 percent of any automaker’s hourly workforce. But first at Stellantis, and later at GM, and finally even at Ford, the UAW ignored that limit and let the automakers exceed the ceiling. That was followed by allowing GM and Stellantis to replace about 10 percent of permanent workers with temps. As a result, at those companies, more than two-thirds of the non-trades UAW workforce is now composed of temps and lower-tier workers (at Ford, it’s about 40 percent). In the crisis of 2007–11, the UAW’s looking the other way on contract violations made some sense; but once solid profitability returned in 2014, this diffidence became unconscionable.

Workers took notice. The UAW’s 2023 “Stand-Up Strike” was, by all appearances, the most class-conscious one in recent memory. Rather than select one of the three “domestic” automakers—GM, Ford, and Stellantis—new UAW president Shawn Fain instead had members at selected plants at all three companies “stand up” when it was their turn. When walking with his members on the picket line, and when at the bargaining table with his Detroit Three counterparts, Fain often wore a T-shirt emblazoned with the slogan “Eat the Rich.” He referred, with some exaggeration, to the company CEOs as billionaires, and repeatedly insisted that, now that the companies, all of which were in or close to bankruptcy in 2009, were profitable, it was “our turn.”

The UAW’s initial demands seemed outlandishly large—a 40 percent wage increase, elimination of “tiers” (in which workers who were hired at about half the top rate didn’t get to it for at least eight years), and even a reduction in the work week to thirty-two hours with no reduction in pay. While the last of these fell by the wayside, the strike won raises that surprised even UAW members: pay gains of 25–50 percent, a shortening of the pay progression from eight to three years, and even a promise that most of these gains would also be implemented in still-to-be-built electric battery and vehicle factories. Unlike the three previous negotiated agreements, this time UAW members voted by large margins to ratify the new contracts. Thanks to the sheer size of the concessions granted during the financial crisis, however—and borne mostly by workers hired since then—even these hefty raises didn’t return the average unionized Detroit Three autoworker to the level of inflation-adjusted pay that they enjoyed in the pre-concessionary 1984–2006 period.

In short, even before any real boost from the Bidenomics investments, very few of which have actually been made, American workers are acting feistier than they have in decades. In 2023, thirty significant work stoppages occurred, involving 465,000 workers and resulting in 16.7 million idle workdays (the most since 2000).26 The UAW’s Stand Up Strike followed several other large, successful strikes, ranging from UPS drivers to Hollywood screenwriters to Amazon warehouse workers and beyond.27 That being said, unions remain small and weak. Despite increased union efforts to organize, year-over-year gains in union ranks remain small. It is unclear if recent union victories can be scaled up and, more importantly, whether those victories can precipitate a new labor-capital-state contract that results in higher productivity and lower costs.

Lessons for Reindustrializers:

Engaging the Workforce to Improve Productivity

This, then, is the crux of the issue: Can Bidenomics, or an America First policy worthy of the name, change the way that U.S. companies do business? Will such policies cause companies to invest more of their own capital, rather than returning it to their shareholders? The near-total lack of performance-related conditions in the three Bidenomics bills is a bad omen, but there is still time to remedy the situation. The three Biden bills make $12 billion available to the Detroit Three to build EVs and their batteries. Why not condition its provision on enforceable commitments to build a minimum number of plants making a minimum number of batteries and EVs by 2028? It’s certainly not a novel concept: the Marshall Plan imposed such conditions on France and Germany; the United States placed such conditions on its 1979 loan guarantee that saved Chrysler; and the Chinese regularly make examples of CEOs who tap public support to enrich themselves rather than the nation. The concept is, after all, utterly capitalist: if we are to put our taxpayers’ money at risk, do we not have the right to expect a proportional reward?

Yet even assuming some modest decoupling from China and the American state’s ability to catalyze domestic productive capacity additions, there remains the question of cost. The Asian mercantilist model has come to be rooted in scale and technology, but it began with—and continues to enjoy (or in the case of Japan, enjoyed until about 2000)—advantages from lower pay and, in China’s case, lower material costs resulting from weaker regulation. That probably means that the lowest ends of traded-goods markets—like mass-market apparel, cheap PCs, very small cars, and commodity steels—will remain dominated by production in Asia (and perhaps someday India and Africa as well). But the United States is a comparatively rich country, so perhaps two-thirds of its markets for manufactured goods are available at our current factor costs for capital, labor, energy, materials, and land. But to keep it that way, and to push that two-thirds to three-quarters or more, our producers will need to achieve significantly lower unit costs for the products they make and sell here.

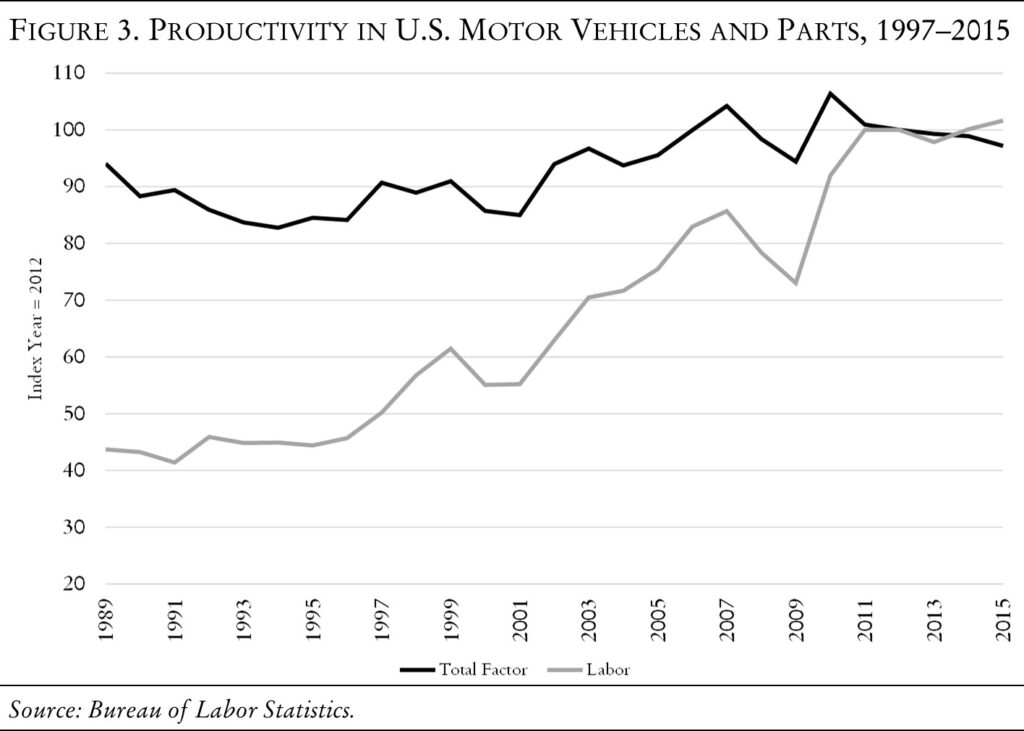

One obvious way for American manufacturers to reduce production costs would be to invest heavily in R&D and fixed industrial capital. But that alone probably won’t be enough. Prior waves of willy-nilly substitution of capital inputs for labor inputs generally ended badly. Of course, even at constant output, the reduction in labor input showed up as higher labor productivity (LP). But total factor productivity (TFP)—that is, accounting for all of the factor inputs—typically flatlined when this approach was followed. In the automotive sector, the biggest wave of capital-for-labor substitution occurred between 1987 and 2015. But during that period, while labor productivity grew by 132.5 percent, total factor productivity grew by just 3.4 percent, suggesting that productivity growth attributable to other factors (mainly capital and materials) was strongly negative. This explains the anemic automaker and supplier profitability of this era: the automakers paid more for materials (including parts) than when they’d made them in-house, partly because suppliers’ prices had to reflect their higher cost of capital versus what the automakers enjoyed.

And beginning in 2011, when the automakers started to bring on new hires at the much lower wages permitted in their revised contracts with the UAW, even labor productivity flatlined, thanks to a less experienced workforce and the erosion of shop-floor solidarity and learning that resulted from having (in today’s terms) $15- and $30-an-hour workers doing the same jobs, with the latter fighting for less mandatory overtime and the former trying to get every work-hour they could.

Despite the fact that dumping union labor and outsourcing parts-making turned out to be an expensive, ineffective approach, most American manufacturers keep doing it. The recent strike wave in the United States holds promise for a more engaged labor movement, but any such upsurge remains immature and will inevitably be prone to a syndicalist emphasis on intra-firm distribution rather than addressing the larger economic and political tasks ahead.

A useful labor resurgence must overcome not just worker cynicism and individualism but also corporate management’s habit of opposing unions. It must defeat the bankrupt idea—accepted as fact by opinion-leaders in both major U.S. political parties—that class conflict is bad for economic growth.

The HR literature advances a number of plausible hypotheses linking unionization to productivity. Chief among them is that union membership lowers employee turnover because it usually provides workers with better wages, benefits, and greater protection against arbitrary discipline and discharge.28 But this kind of union advantage is just the tip of the iceberg of what’s possible if and when union members engage.

To put this in a longer historical context, we can look at the work of one of the first economists to rigorously and quantitatively study the issue of macro productivity in the early postwar period. John W. Kendrick worked as an economist from 1946 to 1953 at the Office of Business Economics, the predecessor to the U.S. Bureau of Economic Analysis; later, he was economics professor at George Washington University.29 In 1980, he argued that, in the postwar period, well-managed companies should share about 60 percent of total factor productivity gains with labor. Sharing more than that could endanger the profits required to reinvest in the business; sharing less would increase inequality with no justification, leading to costly labor strife. Kendrick also noted that, by his definition of productivity, “since the late nineteenth century, the secular rate of growth in real gross product per labor hour in the U.S. domestic business economy gradually accelerated from about 0.5 percent a year to a maximum average annual rate of 3.5 percent in the subperiod 1948–66. Since then, it declined to about 1 percent during the period 1973–78. . . .”30 It is worth noting that the 1948–66 period was one of high unionization, with frequent local and national strikes. Paradoxically, such labor militancy can be harnessed to the benefit of both companies and workers.

Many manufacturing managers, especially those in the trenches on the shop floor, and especially those in industry before 1980, know that conflict is not inconsistent with productivity growth and cost reduction. In the 1980s, Detroit Three executives began to classify each of their remaining factories as being either cooperative or “bad boy” plants. As the companies diverted more and more of their earnings to shareholders, and their market share continued to decline, they responded by closing more and more of their plants. Bad boy plants, of course, were the ones more often closed: if there was too much production capacity, why not shed it where the workforce was most militant? But the data coming in from bad boy plants slated for closure startled the executives: they sometimes exhibited the lowest costs and highest quality among the automakers’ facilities. Moreover, when lower-level managers were consulted about this apparent anomaly, they revealed that these plants had been high performers all along, not just after their workers learned they were about to lose their jobs.

Why would that be? Think about what one might call the production economy—the millions of jobs in which a series of tasks must be executed with a high degree of repetition. This sector includes not only factory work, but much of the service economy: medical coding, processing insurance claims, making appropriate referrals in social service agencies, changing the oil in cars, etc. While there is a great deal of routine, there is also high variance in how much care, attention, and effort workers put in. Particularly when rewards are paltry—as they have been for most such workers since the late 1970s—a large proportion of workers can be expected to figure out ways to do as little as possible without being terminated. (Think of a classroom of students who know what it takes to get a C rather than an F, and who don’t see any great advantage in expending the effort required to get an A.)

Even when compensation is decent, if increases in pay or other valued benefits (e.g., time off) are not visibly tied to worker, department, or workplace performance, the incentive to expend effort and stay engaged is weak. This is how capitalism is supposed to work, as the Milton Friedman quotation at the beginning of this article would suggest. Labor is a key factor input. For it to benefit, labor must be able to advocate for a return on its efforts, just as capital insists on one. Without the local union contract (and, therefore, in nearly all nonunion plants), workers have had no recourse but to disengage and withhold effort, with the unfortunate productivity results we’ve already described. For labor to advocate for a return on its effort, it requires voice—a way to express its concerns and suggestions—and empowerment, a collective institution that has the skill and daring to make that voice protected, understandable, credible, and unignorable.

In this context, the Japanese HR model emulated by U.S. firms since the early 1980s can be seen as a clever (though, in retrospect, cynical) workaround. Rather than reward effort and engagement with money, this approach favored grafting a set of new worker-management interactions on top of an unchanged compensation structure: set up quality circles, organize workers into teams, have workers and managers share parking lots and cafeterias; rename workers as “associates” or “technicians”; listen to their views on which first-line supervisors are despotic and unreasonable. For a while, these workarounds sometimes bore enough fruit to produce compelling anecdotes, but the HR literature of the time produced virtually no quantitative evidence that the cooperationist approach yielded lasting gains in productivity or, therefore, reductions in product or service costs. Even where cooperationism was rigorously attempted, it turned out not to have legs: very few workplaces have such programs in more than name only; and the idea that labor policy even matters has fallen into such disrepute that many employers, large and small, have outsourced most or all of the HR function to outside companies that use cookie-cutter algorithmic approaches to hiring, benefits administration, discipline, and termination.

New Strategies

Today, having lost confidence in the promise of HR gimmicks, as well as simply replacing labor input with more capital input, we must search for and experiment with new approaches to counter the existential threat from the BYDs of the global market.

One area of focus must be design. Understanding Tesla’s single-decade takeover of the U.S. car (though not truck) market and of BYD’s success in building high-quality EVs for about one-third of the cost of established Western automakers offers some important lessons. For example, nearly every vehicle built by American and European automakers uses one of two basic structural architectures: a body-on-frame architecture for most trucks and nearly all pickup trucks, and a so-called unibody architecture for all cars and most utility vehicles. Both feature a structure composed of roughly fifty stamped metal components that are welded or bolted to each other and to which the outside panels of the vehicle—its “skin”—are attached. In most Teslas and BYDs, however, those fifty-odd body structure components are replaced by just two parts known as gigacastings, each a single molded aluminum frame made up of a few vertical and a few horizontal spans. The initial cost to design and mold a gigacasting is substantial, and therefore competes with other uses of capital (including dividends and share buybacks), but the ultimate impact on vehicle cost is massive. Fifty stamped components don’t need to be bought from suppliers and stocked for future accident repairs. The body structure for vehicles with different body shapes can be modified by tweaking the computer programs that guide gigacasting mold-building. Teardowns of Tesla and BYD models have found a number of other cost-saving innovations, all of which share the same economics: more capital up front, measurably lower costs once in production.

Tesla is also militantly anti-union and aggressively fights union organizing campaigns. Not surprisingly, we see weak worker voice there: employees fear reprisals for supporting any form of organization of workers or worker solidarity. This raises another set of questions. As a relatively young company, one branded by the media as a “tech start-up” and led by an idiosyncratic and charismatic CEO, Tesla has not seemed to suffer from a lack of worker motivation or engagement—much like Ford, in broad strokes, in that company’s earliest days. But a much larger question is whether Tesla can continue to maintain a quality, engaged workforce as it matures or experiences changes in leadership, if its current attitudes toward labor persist.

Specifically with regard to labor, some now conventional practices will need to be rethought. Not only has de-unionization failed to restore productivity gains (and perhaps pushed in the opposite direction) in the Detroit Three, it has also revealed a major drawback to what’s called pattern bargaining. In many industries, and particularly in manufacturing and trucking, national unions have sought to negotiate master agreements that apply to all plants of the companies with which the union bargains. Local unions still have agreements covering matters specific to their particular location, of course, but pay levels are almost entirely set by the national pattern. The logic of a national pattern wage for each kind of job was, as the UAW’s longest-serving leader, Walter Reuther, put it, “to take wages out of competition.” But it has had the unfortunate effect of limiting the ability of managers to reward workers for their contribution—arising from the resolution of the conflicts in which they engage—to higher productivity and lower costs. Prior to the 1990s, a portion of workers’ pay could effectively be bargained locally (partly because grievance bargaining and the daily effort-wage bargain could influence the jobs in which particular workers were classified), and there were still a few cents per hour at play locally; but today, there is little leeway for giving financial compensation for cost-saving improvements. To enlist workers in the fight for meaningful cost reductions in traded-goods sectors, that will need to change.31

In short, the sharing of productivity gains and cost reductions within the adversarial collective bargaining system provides a bold policy framework. Productivity bargaining acknowledges the plant knowledge, contributions, and innovations of workers on the shop floor. Based on rigorous analysis of 1970s shop-floor data from the U.S. auto industry, it may show a way forward for unionized companies and their workers.

A New “Hawthorne Works Experiment”:

Labor’s Voice and Productivity

The famous Hawthorne Works study, conducted at the Western Electric Company’s large plant in Cicero, Illinois, was a landmark in American manufacturing history. At its peak, the complex employed forty-five thousand workers and produced consumer goods ranging from refrigerators to advanced communications equipment. Led by psychologist Elton Mayo in the 1920s and ’30s, the study revolutionized our understanding of worker behavior and the dynamics of motivation, job satisfaction, behavioral change, and workplace leadership.32 A pivotal discovery was that workers performed better when they believed they were being observed—a cornerstone of motivation theory. As a result of the Hawthorne studies, there was a renewed emphasis on product quality, employee training, effective supervision, and improving working conditions as overseen unilaterally by management: these touchstones laid the foundation for the human relations movement, which still forms the basis for today’s modern personnel and human resource management practices.

UAW-organized auto plants make for an excellent case study due to a long, well-documented history of local and national collective bargaining, powerful local unions, and a highly developed workforce. While working for eight years as an assembly-line worker at a General Motors plant, this piece’s coauthor Craig Zabala studied collective bargaining at the plant level using participant observation research. In doing so, he came upon data that seemed counterintuitive to academic researchers—namely that shop-floor bargaining had a major impact on plant output and product quality, and that so-called bad boy plants exhibited higher levels of shop-floor engagement, better quality audits, and in most cases higher levels of plant labor productivity. Militant unionism took the job seriously.33 His observations led to significant breakthroughs in how economists, industrial leaders, and academics view productivity performance.

The tug-of-war among plant managers, general superintendents, foremen, and workers—with management trying to get more out of workers than the contract stipulated, and workers likewise pushing back—resulted in fascinating results. Management needed workers to produce at high levels, but because they were organized, the workers would fight to be compensated for doing so. Evidence for their success could be seen in the hourly wage rate differences throughout the plant, which resulted from the to-and-fro of what Zabala called the “effort-wage bargain.”

Zabala took these observations further. He discovered that companies and unions collected historical data on this effort-wage bargain behavior, though they paid little attention to it. He constructed one of the first time-series datasets of shop floor bargaining at General Motors, spanning from the mid-1930s to the early 1980s and including a broad array of metrics—grievance bargaining, extralegal strike bargaining (wildcats, walkouts), absenteeism, quits, quality audits (at the work group, departmental, and plant level), accident rates, and on-the-job deaths. These data had been collected by plant management and the union, and could be augmented with engineering data. Zabala asked how, without using this information, would management know what to do? On what information would it base decisions about which plants to invest in, and which to close?

When Zabala’s plant-level research came to the attention of the U.S. Department of Labor, he was hired to continue this work as part of the Department’s productivity research program. Plant-level productivity research was a missing link in the Department’s microeconomic research program; General Motors and the UAW supported the effort. Within a few years, Zabala entered into a collaboration with John R. Norsworthy, who headed the Division of Productivity in the Office of Productivity and Technology at the Bureau of Labor Statistics. As economists there, Zabala and Norsworthy spent more than ten years exploring whether there might be an alternative labor policy approach that could yield larger and more reproducible cost reductions in the automotive industry and, by extension, in U.S. manufacturing.34 Underpinned by Zabala’s participant observation research, the authors sought to demonstrate empirically how worker behavior on the shop floor affected plant- and company-level economic performance as constrained by company-wide labor policies.

In their economic model of the firm, the moving parts were affected by the actions of workers and their union on the shop floor. Zabala and Norsworthy first built a model to gauge the effects on total factor productivity and the costs of varying levels of capital, labor, energy, and materials inputs in the U.S. motor vehicles and parts sector. Their next step was to construct and stir in proxies for worker attitudes: specifically, plant-level data on grievances (and how quickly they got resolved), authorized and unauthorized strikes, and quits.

With plant performance quantified and rigorously modeled, companies could seek output gains and cost efficiencies and see to what extent they justified sharing with labor. Such an approach, embedded in adversarial bargaining, is not unlike what occurs in negotiations between a firm and its bankers on Wall Street when they work to hammer out acceptable terms for a capital raise or other financial transactions.

Norsworthy and Zabala’s model found quantitative links among worker performance, total factor productivity, and the cost of production. These simulation results overturned a lot of widely held assumptions. Neoclassical economics had always assumed that unions are cost-increasing. Remarkably, this assumption had no measured basis. Prior to the work of Norsworthy and Zabala, the discipline had never measured the output- and capital-augmenting effects of worker behavior in a formal statistical model. The standard microeconomics “theory of the firm,” focused primarily on output measurement and cost accounting, postulated that workplaces and companies were simply a set of more or less identical institutions whose performance and profitability were controlled only by perfect competition, with new firms easily able to enter, and above-normal profits impossible to make. Capital, labor, energy, materials, and technology were assumed to be deployed in the fixed proportions of the production function. Getting past this gross oversimplification required the contribution of shop-floor studies.

Moreover, Zabala and Norsworthy found that the impact on productivity and the cost of varying the firm’s capital inputs wasn’t linear or invariant: it depended on how capital was applied, its cost in the credit markets, and on levels and types of labor-capital conflict. Conflict—measured, as already noted, by grievances, unauthorized strikes, and quits—moved the needle on productivity and cost by requiring negotiated improvements under enforceable local union contracts that addressed the issues over which workers and supervisors were at odds. The contract was a kind of living legal court: most of the conflicts signaled by grievances, walkouts, and so on could be “negotiated to acceptable resolution, some had to be kicked up to higher levels of management, and a few required further concerted action to resolve. Every conflict and every ensuing negotiation was a learning opportunity. Over time, both sides accumulated a growing understanding of which changes advanced productivity and could reward those who contributed to its improvement.”

This shouldn’t be a paradox. To benefit from productivity gains, labor must be able to advocate for a return on its efforts. Without a seat at the negotiating table (typically provided by local unions), workers have no recourse but to disengage and withhold effort, with unfortunate results that make the chances of rebuilding American industry unlikely.

The shop-floor data that Zabala used was laser-focused on production-related issues. Other correlates of worker attitudes and factory-floor bottlenecks could also be discovered and incorporated into engineering models that could then be quickly translated into cost functions. Worker behavior is influenced by variables that include wages and fringe benefits, performance expectations, job security, and health and safety conditions. These variables are labor policy elements and are the constituents of the industrial relations policy expressed in conventional collective bargaining agreements. In the 1980s, however, it was difficult to run simulations even with a relatively short list of model inputs; today, advances in computing, data-scraping, and AI should make running these models easier.

Productivity Bargaining

Historically, total factor productivity has increased more slowly than labor productivity because businesses have replaced labor with capital and other inputs. While this replacement reduces labor costs, it raises the costs of other inputs, in some cases pushing total costs higher. Just as total factor productivity is the right way to measure plant performance in physical terms, the unit cost of production measures plant performance in dollar terms.

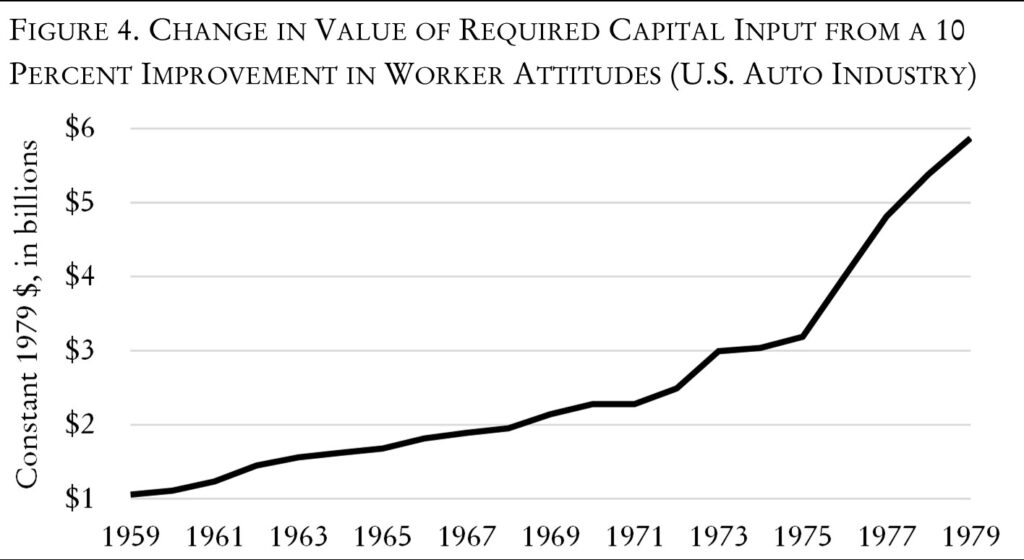

Norsworthy and Zabala simulated the capital savings from a 10 percent improvement in worker attitudes. Since capital is a fixed amount, the value of capital is called a shadow value in their model and associated with constraint. Its value changes if constraints are intensified or relieved, reflecting the marginal value (or opportunity cost) of relaxing or tightening them. Most analysts consider the shadow cost of capital based on borrowing constraints to leverage production (e.g., working capital lines of credit) and compare them to the firm’s user costs. Norsworthy and Zabala introduce worker attitudes as a special type of technical change to see whether and, if so, how much those attitudes constrain capital. They tested a synthetic 10 percent improvement in worker attitudes, measured as a 10 percent improvement in the number (and types) of grievances filed, the grievance settlement rate (fewer unresolved grievances, a better grievance bargaining and settlement environment in the plant), fewer unauthorized strikes, and fewer quits. Unauthorized strikes are typically due to a poor grievance bargaining environment (too many unsettled grievances) or a strike over health and safety. For example, Zabala’s plant had a wildcat strike after a worker was killed when he fell onto the conveyor belt due to unsafe machinery. Workers reacted spontaneously and shut the plant down. New safety policies were negotiated within days, and workers returned to work, but only after the production loss of thousands of vehicles, a terrible and unnecessary outcome of negative productivity bargaining over health and safety exacerbated by months of heavy overtime work.

The simulation results for a 10 percent improvement in worker attitude on the shadow value of capital are summarized in figure 4. The statistical tests found that the shadow values, or implied cost savings, of inputs in the cost function (capital, labor, energy, materials) change significantly with a 10 percent improvement in worker attitudes. Specifically, the shadow value of capital input grew from about $1 billion in 1959 to over $5 billion dollars in 1979; in May 2024 dollars, that $5 billion would have been more than $24 billion in 1977–79. Worker attitudes—and hence the payoff to addressing the sources of withheld effort—became more influential over the time period studied. Consider the implications of this experiment for the ability of big American automakers like GM and Ford to compete with Tesla, BYD, and other innovative low-cost producers. In 1978, roughly 9.5 million cars and light trucks were produced in U.S. factories. In today’s dollars, the Norsworthy-Zabala experiment’s $24 billion in capital saving would have meant that each could have been produced for $2,600 less had there been a 10 percent response to expressions of labor voice. It also means that a company such as Ford, which in 2023 produced almost exactly two million vehicles in its American plants, could have earned, and therefore could have reinvested, as much as $5.2 billion more.

A simple reading of our argument might suggest that highly unionized automakers in the 1970s and 1980s should have been highly profitable. One big reason they were not, of course, is that market share losses to newly capable foreign competitors were sapping their economies of scale. But it was also because the focus of union bargaining was on establishing a national wage pattern rather than addressing stagnating productivity. Both the automakers and the UAW International in Detroit strongly opposed giving local plants more power to negotiate, fearing it might cost them control of national bargaining. And particularly after 1980, the UAW was laser-focused on minimizing national contract concessions, and its leadership was in no mood for local union militancy or problem-solving. Nor was that leadership aware of the root causes of the employers’ productivity doldrums: not since the early 1960s had the UAW made any serious attempts to get the automakers to share their production or financial data. The result was a major lost opportunity to maximize factor inputs and slash costs to address the emerging competitive horizon.

The productivity bargaining needed to achieve the kind and level of results found in the Norsworthy-Zabala experiment would require the company to open the books at the plant level for transparency, accuracy, and accountability as new policies related to production are designed and implemented by both management and labor. Pattern bargaining, which takes place primarily at the national union and corporate levels, rather than at the plant level, cannot produce comparable results. Productivity bargaining draws attention to interfirm and interplant differences in productivity gains and cost reductions, and improvements become the basis for sharing gains between capital and labor. Of course, the Norsworthy-Zabala results were only a simulation based on a narrow set of worker voice indicators. Using a much broader set of such indicators, and with companies opening the books to show output and financial information, would likely lead to even larger cost savings being identified and shared.35

Labor’s Role in American Reindustrialization

The challenge from BYD neatly encapsulates the potential for an extinction-level event for American production in the absence of a new model that can deliver huge scale and much lower unit costs. It challenges corporations to reconsider their ruinous habit of stock buybacks and generous dividend payments; it demands that they up their investment game.

To compensate for the excessive sell-off and write-downs of vertical integration and their post-2009 dependency on cheap credit in the capital markets, the programs initiated by the three Biden bills will have to face up to the error of subsidizing investment while imposing no meaningful conditions on the recipients of state largesse. For its part, labor must get bigger, stronger, and above all smarter if it is not only to share in but also to contribute to the big increases in productivity required for large reductions in cost. We judge its leadership to be readier than employers’ and more reliable as partners than the easily distracted and arguably captured state. While simply fighting for a larger share of a pie that soon may be shrunk—this time by formidable China-based competitors—is desirable, it is not sufficient. Unions, and the companies that employ their members, must be players in a comprehensive plan in which union members share in the gains from qualitatively higher productivity. Such a plan, inevitably quarterbacked by the federal government, may well be the only way to reindustrialize America.36

This article originally appeared in American Affairs Volume VIII, Number 4 (Winter 2024): 80–105.

Notes

1 Milton Friedman, “

On Slavery and Colonialism,” in

Is Capitalism Humane? (Ithaca, N.Y.: Cornell University Press, 1978).

2 To quote a recent article, “No country has come close to matching the scale and tenacity of China’s support [for manufacturing]. The proof is in the production: In 2022, Beijing accounted for 85 percent of all clean-energy manufacturing investment in the world, according to the International Energy Agency. . . . Now the United States, Europe and other wealthy nations are trying frantically to catch up. Hoping to correct past missteps on industrial policy and learn from China’s successes, they are spending huge amounts on subsidizing homegrown companies while also seeking to block competing Chinese products. They have made modest inroads: last year, the energy agency said, China’s share of new clean-energy factory investment fell to 75 percent. . . . The problem for the West, though, is that China’s industrial dominance is underpinned by decades of experience using the power of a one-party state to pull all the levers of government and banking, while encouraging frenetic competition among private companies. . . . China’s unrivaled production of solar panels and electric vehicles is built on an earlier cultivation of the chemical, steel, battery and electronics industries, as well as large investments in rail lines, ports and highways.” Patricia Cohen, Keith Bradsher, and Jim Tankersley, “How China Pulled So Far Ahead on Industrial Policy,” New York Times, May 27, 2024.

3 American Society of Civil Engineers, “Overview of Bridges—2021 Report Card for America’s Infrastructure,” accessed June 1, 2024.

4 For example, Ford announced last October that it was “postponing around $12 billion in planned EV investments, including the construction of a new battery plant. The company’s electric unit, called Model e, lost $1.3 billion for the quarter, a loss of about $36,000 per vehicle delivered.” See: Ian Krietzberg, “Former Ford CEO Has a Blunt Warning For the Electric Vehicle Industry,” The Street, October 27, 2023.

5 A particularly important Biden-era regulation requires grid operators’ plans for both generation and transmission to look out a minimum of twenty years. This is driving the major investments in high-voltage power lines that are needed to fully integrate solar and battery storage into the mix. A shorter time perspective would likely lead to underinvestment that would, in turn, retard the share growth of solar and wind.

6 Mark Zandi and Bernard Yaros, “Macroeconomic Consequences of the Infrastructure and Budget Reconciliation Plans,” Moody’s Analytics, July 20, 2021; Joseph W. Kane, “Seizing the US Infrastructure Opportunity,” Brookings Institution, December 2022.

7 For a clear exposition of multipliers (and their frequent misuse by promoters of economic development, see: Timothy Bartik, “What are Realistic Job Multipliers?,” Upjohn Institute, April 24, 2019. For a good summary of multiplier estimates and their derivation by sector, see: Josh Bivens, “Updated Employment Multipliers For the U.S. Economy,” Economic Policy Institute, January 23, 2019. For a good analysis of infrastructure investment’s impact on growth, employment, and productivity, see: Beth Ann Bovino, “How U.S. Infrastructure Investment Would Boost Jobs, Productivity, and the Economy,” S&P Global, August 23, 2021. The sectoral composition of total jobs additions is nicely summarized in Niels Graham, “The IRA and Chips Act Are Supercharging US Manufacturing Construction,” Atlantic Council, February 13, 2024.

8 All three of the bills incorporate the Depression-era Davis-Bacon Act to raise and, more important, to standardize pay across union and nonunion workforces. The IRA goes further, stipulating that if a company produces clean-energy products without also pursuing union-biased apprenticeship approaches, then the value of the tax credits it can claim decreases from 20–30 percent to 6 percent.

9 Bureau of Labor Statistics, “Union Members—2023,” January 23, 2024.

10 Zachary Parolin and Tom VanHeuvelen, “The Cumulative Advantage of a Unionized Career for Lifetime Earnings,” ILR Review 76, no. 2 (October 2022).

11 Craig Zabala and Daniel Luria, “New Gilded Age or Old Normal,” American Affairs 3, no. 3 (Fall 2019): 18–37,

12 Erica Groshen, Cornell University economist and former Bureau of Labor Statistics chief, cited in Nancy Marshall-Genzer, “Workers Used to Earn about Two-Thirds of the Income Their Labor Generates. Now, It’s Just over Half,” Marketplace, April 24, 2024.

13 For a readable summary of the surrender of onshore U.S. semiconductor production, see: Keith Bradsher, “How China Rose to Lead the World in Solar Panels and Other High-Tech Goods,” New York Times, May 15, 2024.

14 “Visualizing 50 Years of Global Steel Production,” FIAR—News, June 29, 2021.

15 Stephen Herzenberg, “The North American Auto Industry at the Onset of Continental Free Trade Negotiations,” Department of Labor—Bureau of International Labor Affairs, 1991.

16 American Public Power Association (APPA), “America’s Electric Power Generation Capacity: 2023 Update,” May 2023.

17 The UAW leadership knows this. The day after Biden walked a picket line with UAW President Shawn Fain, Trump gave a speech at a nonunion Detroit area auto supplier, in which he said that, were Biden to win a second term, any UAW strike gains would be lost in just a few years as the traditional industry is devastated by EVs made in China. It’s true that somewhat less labor is required to make battery cells and packs and electric motors than to build the gasoline and diesel engines, traditional transmissions, and exhaust emissions systems that most EVs don’t need. And until the UAW won its strike, there was a very real possibility that many EVs, and most of their batteries and motors, could be built in nonunion plants. While current U.S. law would deny the most generous consumer subsidies to EVs made, or with batteries made, offshore, Trump’s view that a high tariff on China-built EVs may be necessary to give the emerging U.S. EV sector time to achieve economies of scale has largely been adopted by Biden as well. Never mind, of course, that the domestic automakers could have invested in a share-holding position in batteries and EVs had they not frittered away their profits in payments to shareholders. But Fain has made clear that he thinks climate change is real and the transportation sector is the single biggest source of the greenhouse gas emissions that are driving it. So, for the UAW, the question is not whether or not to oppose or encourage EV purchases; it’s how to build them and their parts here in union shops.

18 Tom Randall, “Slowdown in US Electric Vehicle Sales Looks More Like a Blip,” Bloomberg, May 28, 24.

19 Giles Parkinson, “China Has Won the EV War, and US Car Makers Are Changing Their Electric Plans,” Driven, May 7, 2024.

20 Nora Eckert, “Detroit Three Automakers Should Exit China, Leading Analyst Says,” Reuters, June 18, 2024.

21 C. K. Prahalad and Gary Hamel, “The Core Competence of the Corporation: How Companies Cultivate the Skills and Resources for Growth,” Harvard Business Review (May/June 1990).

22 To quote a recent product review, “BYD is selling “[a] world-class sedan for the people, from China’s biggest name in EVs. It’s here to best Elon’s offering, and it may well be the car to do it. . . . BYD [has] quickly made a name for itself as it expands into Europe. First came the small Dolphin hatchback and the ATTO 3 compact SUV, with both aiming to undercut rivals in a way Korean brands like Kia and Hyundai managed [to do] with great success a decade or so earlier … and just as the Koreans have. . . . BYD [now also] wants to head upmarket. It intends to do so with the Seal, an electric four-door sedan priced from around €45,000 in Europe and £45,000 in the UK.” See: Mark Andrews, “Review: BYD Seal 2024,” Wired, April 22, 2024.

23 Interestingly, German automakers are hostile to EU tariffs on Chinese EVs. This is not surprising: they depend on sales in China for a plurality of their global revenue and profit.

24 “How Worrying Is the Rapid Rise of Chinese Science?,” Economist, June 15, 2024.

25 Peter Johnson, “BYD Is Now the World’s Largest Automaker by R&D Workforce after Major Hiring Spree,” electrek, September 13, 2024.

26 Drew DeSilver, “2023 Saw Some of the Biggest, Hardest-Fought Labor Disputes in Recent Decades,” Pew Research Center, January 4, 2024; cited in Arthur MacEwan “What is the State of Organized Labor?,” Dollars & Sense (May/June 2024).

27 DeSilver, “2023 Saw Some of the Biggest, Hardest-Fought Labor Disputes in Recent Decades.”

28 See, among many others, the ILR Review symposium on Richard Freeman and James Medoff, What Do Unions Do? (New York: Basic Books, 1984), in ILR Review 38, no. 2 (January 1985).

29 John W. Kendrick, “U.S. Productivity in Perspective,” Business Economics 26, no. 4 (October 1991).

30 John W. Kendrick, “Survey of the Factors Contributing to the Decline in U.S. Productivity Growth,” Boston Federal Reserve, 1980.

31 To be clear: we are not arguing that all of the cost savings from every improvement that results from the resolution of local workplace should go to workers as additional compensation. This is capitalism, after all. Even a few more cents per hour speaks to the bargain that workers, as human beings operating in a market economy, expect: “You want more from me? OK, but what’s in it for me?” In the postwar United States until about 1980, it was a rule of thumb that about 60 percent of productivity gains went toward enhancing workers’ compensation. John W. Kendrick’s 1991 article, cited in the previous footnote, looks at U.S. productivity growth for the period 1889–1998 and comments on the well-documented productivity slowdown from 1973–81. See: Samuel Milner, “The Problem of Productivity: Inflation and Collective Bargaining after World War II,” Business History Review 92, no. 2 (Summer 2018): 227–50. The 60 percent figure makes a lot of sense, since labor income in the period accounted for about two-thirds of national income and GDP. Since 1980, on average, labor compensation has captured no more than about 20 percent of productivity gains, the rest split between owners of capital and consumers.

32 Elton Mayo, The Human Problems of an Industrial Civilization (London: Routledge, 2004).

33 Many managers understood this and didn’t buy into the post-1980 union-busting prescription. “[When] asked which way they would like to see their own companies’ collective bargaining go in the future—toward a return to traditional negotiation or toward forcing concessions from labor, ‘even to the point of eliminating the unions’. Among executives of companies that are heavily organized and accustomed to dealing with entrenched and sophisticated unions, there is little incentive for pressing current gains. By a margin of 66 percent to 23 percent, these [managers] are anxious to return to traditional bargaining practices …. As [pollster Louis] Harris comments, ‘These people don’t expect to get rid of unions and figure that they might as well work with them.’ . . . [Managers] in companies with relatively little unionization split almost equally on whether to return to an adversary relationship.’” See: “A Management Split over Labor Relations,” Business Week 14 (June 1982): 19.

34 The articles detailing this ten-year journey include, in reverse chronological order: Craig A. Zabala, “Sabotage at a General Motors Plant,” in Autowork, eds. Robert Asher and Ronald Edsforth (Albany: State University of New York Press, 1995), 209–25; Alice C. Lam, J. R. Norsworthy, and Craig A. Zabala, “Labor Disputes and Productivity in Japan and the United States,” Studies in Income and Wealth, vol. 53 (Cambridge, Mass.: National Bureau of Economic Research, 1991): 411–35; J. R. Norsworthy and Craig A. Zabala, “Worker Attitudes and the Cost of Production: Hypothesis Tests in an Equilibrium Model,” Economic Inquiry 28, no. 1 (January 1990): 57–78; Craig A. Zabala, “Sabotage at General Motors’ Van Nuys Assembly Plant, 1975–1983,” Industrial Relations Journal 20, no. 1 (Spring 1989): 16–32; Craig A. Zabala, “Information Systems and Labor-Management Cooperation: Negotiating for Productivity Improvement and Cost Reduction,” U.S. Department of Labor Bureau of Labor-Management Relations and Cooperative Programs, 1990; J. R. Norsworthy and Craig A. Zabala, “Responding to the Productivity Crisis: A Plant-Level Approach to Labor Policy,” in Productivity Growth and U.S. Competitiveness, eds. William J. Baumol and Kenneth McLennan (Oxford: Oxford University Press, 1985), 103–18; J. R. Norsworthy and Craig A. Zabala “Effects of Worker Attitudes on Production Costs and the Value of Capital Input,” Economic Journal 95, no. 380 (December 1985): 992–1002; J. R. Norsworthy and Craig A. Zabala, “Worker Attitude, Worker Behavior, and Productivity in the U.S. Automobile Industry, 1959–1976,” Industrial and Labor Relations Review 38, no. 4 (July 1985): 544–57; J. R. Norsworthy and Craig A. Zabala, “A Note on Introducing a Measure of Worker Attitude in Cost Function Estimation,” Economic Letters 10, no. 5 (October 1982): 185–91.

35 Absenteeism is an obvious candidate to add to the roster of indicators. The data collected by Zabala showed increasing worker and local union militancy throughout the period 1976–79, with significant increases in grievances filed and in grievances not yet settled by plant managers and union representatives. Intensifying shop floor bargaining represents increasing worker engagement. Absenteeism was also increasing after 1975, as GM overtime set postwar records; in Zabala’s plant, where he worked on the door line in the body shop, nine-hour workdays and two Saturdays a month were standard production schedules from 1976 to 1980. That absenteeism was to be expected, as missing work gave workers some control over their life and take-home pay was ample; Zabala referred to this as counter-planning on the shop floor.

36 This should not be a controversial position: Adam Smith could never have foreseen that three American billionaires would have more wealth than the bottom 50 percent of the population; had he done so, he would have seen it as a predictor of societal demise and not of capitalist success. As Milton Friedman reminded us in the quote that opens this article, a fully functioning neoclassical model of the firm requires that all factor inputs engage in profit-maximizing behavior. In today’s environment, in which the working class has been demoralized and in which unions represent only 10 percent of the U.S. workforce, labor’s ability to play its necessary role is badly damaged. This has bequeathed to us a sclerotic economic system, which can only be rejuvenated by more labor-management conflict, the application of scientific rigor to estimating how responses to conflict can boost productivity (especially the productivity of capital), and a state that invests heavily and intelligently in rebuilding American industry as it did leading up to and during World War II, and as China has done since 1990.