Stagflation: Causes and Cures

Few today will dispute that inflation is a serious problem. The latest CPI number, from April 2022, came in at 8.3 percent. Core inflation clocked in at 6.2 percent. Although slightly below the highs of March, the last time we saw inflation numbers like these was in the early 1980s.

What is even more shocking is that this inflation does not seem to be a simple case of economic overheating. In the first quarter of 2022, CPI averaged 8 percent and yet real GDP contracted by 1.4 percent. In basic macroeconomic theory, inflation is the result of too rapid growth in the economy. But if the economy is contracting at the same time as inflation is high, it is possible that the economy is slipping into stagflation.

Inflation versus Stagflation

Stagflation is a situation in which economic growth is low and inflation is high. It is the worst of all possible worlds. Income grows slowly, unemployment increases significantly (although we have yet to see this at the time of writing), and prices continue to rise. The last time we saw stagflation was in the 1970s.

Stagflation is also punishing for savers. In an inflation driven by high economic growth, firms earn more money as economic activity is high. This is reflected in the firms’ stock prices and dividend disbursements. Not so in a stagflation, in which markets tend to underperform and all wealth, asset and monetary, is eroded.

Normal inflation and stagflation have different causes. As we have already said, normal inflation is driven by too rapid economic growth. In economics-speak, we say that aggregate demand in the economy is outstripping aggregate supply. Think of aggregate supply as the total number of goods and services that are available for purchase by consumers and producers. Aggregate supply grows as firms invest in the economy. But there are limits on this growth. Aggregate demand, on the other hand, is the total amount of spending in the economy. There are no theoretical limits on the growth of aggregate demand. An increase in loans—public or private—can increase aggregate demand without increasing aggregate supply. This can lead to inflation.

Stagflation involves the supply side of the economy. In rare instances, we see a large amount of aggregate supply wiped out. One famous example of this is the case of Zimbabwe: After Robert Mugabe seized power, he expelled and harassed the white farmers. But when they left, he found that the black workers did not have management experience in running the farms. The result was a collapse in Zimbabwean food production and very high inflation.

The 2020–22 Collapse in Aggregate Supply

Economists call examples like Zimbabwe “supply shocks.” Many are not as extreme as the case of Zimbabwe and so do not lead to much inflation. But recently, we have seen a lot of very large supply shocks. The first were the lockdowns that various governments undertook in response to the outbreak of Covid-19. These lockdowns had a brutal impact on the supply-side of the economy. They interfered with factory operation and maintenance, placed restrictions on trade and commerce, prevented new truck drivers from obtaining training and licenses—the list is endless. We did not notice the impact on the economy as we sat in our homes, but the supply side was withering on the vine like an unpicked grape. We are now seeing the results of this with food processing plants, for example, experiencing industrial accidents at a very high rate, disrupting the food supply.

The lockdown was probably a sufficient supply shock to generate some stagflation. But it was followed by an even worse supply shock: the war in Ukraine. The war has led to a seizing up of world energy and commodity markets. These started with the trade sanctions that the NATO countries imposed on Russia. The sanctions rested on the assumption that Russia is a small, weak economy—only the size of Italy, we are often told—and that the more prosperous countries could crush it, as they previously crushed the economy of Iran. But what we have subsequently found is that, while Russia may be relatively small on a pure GDP basis, it has an enormously disproportionate impact on markets for commodities and energy.

The Russians appear to know this. If you follow Russian media and war commentary, you will often hear commentators scoff at GDP numbers as “fake statistics.” Instead, they argue, the production of hard commodities—the stuff that makes stuff—is where the power lies. As a macroeconomist who sees something strangely beautiful in the construction of GDP metrics, I am somewhat ruffled by the Russian view. But it is hard not to admit that they have a point. The barrel of oil handed over for $100 is fundamentally different from the $100 squandered at the casino. Yet GDP counts them all the same.

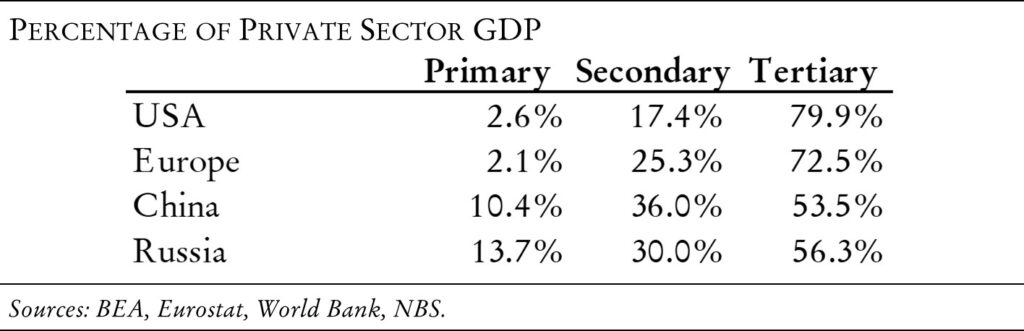

Economists call energy and commodities “primary products”—in contrast to “secondary products” (manufactured goods) and “tertiary products” (services). The clue is in the name: you need primary products to make secondary products, and primary and secondary products to make tertiary products. Primary products are therefore more fundamental to the economy than are secondary and tertiary products. Tertiary products are easily replaced. Secondary products are harder, but not impossible. Primary products are almost impossible. The table below shows the primary, secondary and tertiary sector as a percent of private sector GDP for the US, Europe, China, and Russia.

As we can see, the fully developed economies of the United States and Europe look fundamentally different in their structure than the economies of China and Russia. The former are dominated by their service sectors and maintain mid-sized manufacturing sectors, together with very small commodities sectors. Russia and China, on the other hand, have very large manufacturing sectors and substantial commodities sectors. These simple statistics give us some sense of why the sanctions the West has tried to impose on Russia have resulted in large-scale shortages and stagflation in the Western economies.

A somewhat amusing illustrative example that shows how the sanctions have backfired comes from the Donbas itself. As part of the Western sanctions, various Western companies pulled out of Russia. One of these was McDonalds, which paused it operations in Russia immediately after the invasion and subsequently pulled out permanently. But the Russians refused to shut down their McDonalds. The restaurants themselves were run by Russians and the food products sold were sourced in Russia. So they just rebranded the restaurants and kept operating. In the Donbass, the Russians renamed the chains DonMak and burgers with the new branding were soon popping up next to Kalashnikovs on Russian propaganda channels.

Contrast the DonMak saga with what is happening elsewhere. Policymakers are concerned about food shortages the world over. Energy prices have spiralled in Europe and America. Raw materials for production have become ever more expensive. Rebranding McDonalds is not stagflationary; messing with the markets for primary products is. Russia’s economic dependence on the West is mainly in its relatively small tertiary sector and some technology products. But many of these services are quite literally Western-in-name-only and can be retooled overnight. One suspects that the same is true in China.

Managing Inflation versus Overcoming Stagflation

The solution for normal inflation is simple enough: reduce economic growth. Or, to redeploy the economics-speak we learned earlier: to lower aggregate demand relative to aggregate supply. This eases the pressure on the supply side of the economy and prices cool. The most common way to do this in modern times is for the central bank—in America, the Federal Reserve—to raise interest rates.

There is a lot of silliness written about central bank policy in our day and age. Much of this is propaganda to cover up what central banks actually do when they engage in inflation control. The actual practice involves raising interest rates until the economy enters a recession. Interest rates represent the price at which firms can borrow money to increase investment (and households can borrow to fund consumption). As the interest rates rise, the price of investment rises, so less is undertaken. At a certain tipping point, investment reverses, the economy stops growing, workers are laid off, and the economy enters a recession. Most of the jibber jabber you hear about interest rates seeks to sweeten this harsh medicine and pretend this is not the goal. But it is.

Yet as we have seen, stagflations are not primarily driven by too much aggregate demand. If prices are rising in, say, Zimbabwe because food production has been wiped out, central bankers monkeying with the interest rate is unlikely to have much of an impact. Likewise, if inflation in our economies is due to a supply side rotten from the pandemic and out-of-control primary product markets, then raising interest rates may not have much of an impact. Easing aggregate demand may give the supply side a chance to heal itself—though, alternatively, it could result in falling firm revenues and reduced investment in productive capacity, which then worsens the rot.

A new approach is needed, one that goes beyond short-term interest rate management. In a narrow sense, it may be possible to manage inflation simply by raising interest rates enough to provoke a sufficiently deep recession, but the cure may be at least as bad as the disease, and it does not address the underlying causes of stagflation. Overcoming stagflation in the 1970s involved not just the Volcker shock to interest rates but also Ronald Reagan’s “supply-side reforms” (as well as an oil glut and lower commodity prices). Supply-side reform is also required today, though the simple 1980s model of cutting taxes, as evidenced by the limited impact of the 2017 Tax Cuts and Jobs Act, is unlikely to get the job done. Instead, the United States needs to pursue a longer-term strategy of rebalancing primary and secondary production—in other words, better managing its trade policy.

The Victorian Model

To get our bearings, it is helpful to turn to an empirical example from the past. Victorian Britain during its golden imperial period stands out as an apt point of reference. This period shows that managing trade policy, not tinkering with short-term interest rates, used to be the basis of successful economic policy.

During this period, Britain saw itself as a trading nation. It stitched together an awesome economic machine the likes of which the world had never seen before. Much of this was based on the colonial relationships it established in this century. Britain’s imperialist model was based on manufacturing and finance. Britain would acquire raw products from its colonies, it would then remake these into finished goods in its factories. Most of these goods would be sold in Britain, but some would be sent abroad—including back to the colonies—and the loans that were required to buy these goods would be facilitated by the financial center in the City of London. This made British sterling the de facto reserve currency of the colonies, further stitching them into the imperialist relationship.

Ingenious as the British imperialist system appears, it did not emerge through a concerted plan. Rather it emerged organically, out of the small-scale ingenuity of British people working in a variety of sectors, from government to banking to colonial administration to trade. But the relationships that emerged ensured that British policymakers were very aware of the importance of their trade policy. For this reason, trade policy became the obsession of government. The Victorians would fret about trade policy the way policymakers today fret about government finances and interest rates.

Focusing attention on trade proved to be effective. Throughout the golden period of British imperialism—that is, between the reintroduction of the gold standard after the Napoleonic wars in 1821 and the beginning of the Long Depression in 1873—Britain mostly ran trade surpluses. Some of these trade surpluses flowed naturally to the Exchequer and the result was also consistent government surpluses. This can be seen in the chart below.

It was not just the public and external finances that were stable. British financial markets in this period were also a picture of tranquility. During this period the yield on consols—that is, perpetual bonds—never rose above 4 percent and never fell below 3 percent. The bond market was never seen as a tool of active economic policy. Rather, it was seen as somewhere for savers to park their money and where people living on fixed incomes could derive their earnings. In this model, interest rate policy is not seen as some quick-fix technocratic plaything, but rather an outcome of successfully managing underlying economic phenomena—namely, the trade balance.

A New Policy Outline

Needless to say, the Victorian period is very different from the current situation. Among other things, America is not managing “colonies” and long ago ceased to be the world’s dominant manufacturer. But Victorian Britain provides a useful political model—reminding us that economic policy used to mean more than hoping the Fed’s models are right. In that spirit, we should stop paying attention to metrics that mean little—like the government financial balance—and focus on metrics that mean a great deal—namely, the trade balance. While such an approach cannot be fully articulated in one article, a basic sketch of an anti-stagflation agenda could look something like the following.

The first and most important plank of the strategy aims at reducing import dependence. Before the lockdowns, imports to the United States were almost 15 percent of total GDP. Consider that in the 1950s and 1960s, they were less than 5 percent of GDP. The United States should set a short-term target of 10 percent for imports and a medium-term target of 7.5 percent. This will be achieved through import substitution. One way to pursue import substitution would be for the United States to set up an import substitution bank, which will issue bonds that will be bought by the Federal Reserve. The bonds will have a permanent zero interest rate and should be perpetual. The Federal Reserve will then staff the bank with analysts and economists who will identify products being imported from abroad that could realistically be made in America (say if labor costs were lower). The bank will then subsidize domestic companies so that they can compete with foreign companies. These subsidies should be regularly checked, rechecked, and altered according to circumstance. The budget for the bank should be set by the Federal Reserve in accordance with the time horizons of the goals in question. Of course, both the design and execution of such a project are immensely complex issues, and this brief outline should not be interpreted to suggest otherwise. But the basic principles of import substitution will have to be brought to bear.

The second element of this strategy is simply stamping out inflation. This should be done through large interest rate shocks, as we previously saw under Federal Reserve chairman Paul Volcker in the late 1970s and early 1980s, and interest rate increases are now underway. These shocks will generate a recession. To ease this recession and further reduce prices, the import substitution bank should temporarily commit to increasing its subsidies on all goods until the recession is officially over. This will ease burdens on the American people while further driving down domestic prices.

To make sure that the stagflationary vampire is dead, we should drive an additional stake into its heart. To achieve this, we will work on the consumer psyche. The Federal Reserve will commit to issuing a new dollar. One U.S. dollar will be worth 10 cents in new dollars. The Federal Reserve will gradually phase in the new dollar and phase the old Dollar out, much in the same way the European Central Bank phased in the euro. As the currency is being phased in, retailers will have to list dual prices and accept both currencies. This technique has been used in other countries after severe inflations and was enormously successful in anchoring consumer inflation expectations. It is also good in itself. Bringing back the nominal value of a dime should strike any but the coldest among us as a noble cause. It could also lift national spirits, reigning in a new period of strength and stability.

These new strategies will give policymakers an opportunity to completely overhaul our central banking systems. For too long, central banks have become playthings for Wall Street speculators. Anyone who has watched the unseemly dance between speculators and central bankers cannot but feel a little nauseous. After we have gotten stagflation under control, we should completely overhaul the mandates of central banks. They should still be allowed to hike interest rates when inflation gets seriously out of control. But their day-to-day policy goal should be to set a “fair rate” of interest that compensates savers for saving. This fair rate should be equal to the annual rate of growth of labor productivity—that is, the “natural” rate of economic growth at full employment. This turns central bank policy into a means to ensure fair distribution of resources as opposed to the hurly-burly of cyclical management.

At the same time, we should overhaul how we talk about the economy. Since the Second World War we have tended to obsess over government deficits. But these are far less important than trade deficits, which we have tended to ignore. It is trade deficits, not government deficits, that have led to our present quandary. For this reason, we should train our policies to obsess over trade deficits and how to fix them. This effectively sends economic policy back to where it was in the nineteenth and early twentieth century, when politicians largely ignored the government balance sheet and focused on the country’s balance sheet—a far healthier state of affairs.

It is becoming increasingly clear that the Western postindustrial nations have underappreciated vulnerabilities vis-à-vis the rest of the world. Globalization has caused us to become heavily dependent on others, including geopolitical rivals, for much of our prosperity and stability. Major conflict between world powers, like what we are currently seeing in the Ukraine, poses enormous economic dangers to us. We can rebuild from this position of weakness, and we should. But our foreign policy establishment needs to understand our weaknesses in any economic war immediately. They are operating under assumptions that have not been true for twenty or thirty years, while economic policymakers seem incapable of focusing on the supply side of the stagflation threat.

Clearly what I am offering is not a quick fix solution. But it is quick fix solutions that have gotten us here. Quick fix solutions to complex economic problems, quick fix solutions to complex geopolitical problems—if someone comes bearing a quick fix solution policymakers should be skeptical. What I am offering is an ambitious strategy, which will take effort and time to implement, and which will require patience to assess. Such a strategy is not optimized for a social media age. But following the hysterical herd has gotten us in this mess. Now is the time to try something else.