John Maynard Keynes recognized that countries with persistent current account surpluses posed a threat to the world economy, but no agreement was reached at Bretton Woods, nor in any subsequent discussions, on how countries might be dissuaded from running them. The burden of accommodating or altering these imbalances thus falls on the deficit countries, and what has for many years been a chronic problem has now become acute. Demand matches supply worldwide but not necessarily for individual economies. Countries that seek to save more than they invest have inadequate internal demand and, if they invest abroad, this depresses their exchange rates, allowing those with weak domestic demand to avoid unemployment by exporting more than they import.

Countries run trade deficits because investing in such countries appears more attractive than elsewhere, in terms of the expected returns and risks. The exchange rate that results produces the trade surpluses and deficits that match investors’ preferences. As with all market prices, exchange rates reflect the short-term equilibrium, because buyers and sellers must match, but exchange rates are unstable as both trade flows and investor preferences are constantly changing. It is, however, easier to change the prices of currencies than the flows of goods and services. So trade responds more to exchange rates, which move with changes in international investment preferences, than exchange rates do to trade.

Exchange rates fluctuate, and their changes are often ephemeral, so the experience of traders encourages feedback loops which introduce considerable short-term instability in currencies. Accurate forecasting seems impossible, because, without the benefit of hindsight, we cannot distinguish ephemeral wobbles from fundamental alterations in investors’ preferences. The theory that exchange rates must in the long-term adjust so that currencies have similar purchasing power is reasonable, but it provides little help to forecasters for two reasons: mispriced currencies can adjust through variations in comparative inflation rates as well as exchange rates, and the equilibrium rates vary with relative rates of productivity.1

The United States has run current account deficits every quarter since Q2 1982. These deficits have been too large and persistent to be ignored, or sensibly attributed merely to the commercial importance of the dollar, even though it is claimed that three-quarters of world trade is invoiced in dollars.2

The world has been happy not only to denominate its transactions in dollars but to hold U.S. assets rather than those of other countries. If the same returns are expected in all countries, investors will favor the one where they perceive the risks to be lowest. Investors’ preferences change as expectations vary, but the country where risks are lowest will still on average have a currency that is overvalued by other criteria. The United States has been perceived as a safe haven for assets, just as China has provided the opposite example. Chinese companies and their rich owners wish to diversify their assets so that they are not all at risk from arbitrary government expropriation. The U.S. deficit is particularly high when it reflects the pull of above-average expected returns as well as low perceived risks, while China’s surplus reflects the weight given to the perception of risk even when expectations for returns are not depressed.

From Chronic to Acute

As the problem of trade imbalances has moved from chronic to acute, the authority of consensus economics, which provides the arguments against trade barriers, has collapsed. The proximate cause for macroeconomics’ loss of status is the relationship between trade and fiscal imbalances, and its fundamental cause is the failure of consensus economics to offer, let alone provide, solutions to the problems presented by these connected deficits.

Efficient production in one place leads to rusting equipment in another. Trade heightens competition and provides bad political publicity when foreigners appear to win. From the end of the colonial era to World War II, the United States was mostly a high tariff country but grew so well that its success has been used as supporting evidence by opponents of free trade. Growth was, however, even more rapid and accompanied by lower trade barriers for many years after 1945. But the postwar period of low U.S. tariffs is now over and the instinctive response from other countries, as France’s protective attitude over European rearmament has shown, is often to amplify rather than ignore the impact.

We are witnessing a change in one of the accepted principles that determine policy, which is unlikely to be reversed. It is the change of attitude that matters rather than the details of tariff negotiation. Concessions made to reverse higher tariffs risk encouraging further threats. “You can pay Danegeld, but you cannot be rid of the Dane” has been a common response to the UK’s trade concessions in the face of high U.S. tariffs on steel and cars. It refers to Anglo-Saxon England’s failed attempt to stop Danish attacks by paying blackmail. In negotiations between two countries, the weaker one cannot expect deals to be final unless shame is part of the stronger one’s psychology.

Countries have trade deficits when they spend more than their income and budgets; fiscal deficits have the same characteristics for governments. Their close connection, however, only becomes obvious when they are large. Keynes showed that unconventional policies were needed to prevent massive unemployment when the private sector seeks to save more than it invests. The solution is for governments to run budget deficits that reduce the economy’s total savings and bring them into balance with intentions to invest. These deficits are only necessary on those occasions when interest rates are so low that further cuts fail to boost demand and are labeled “liquidity traps.” While Keynes’s analysis is an accepted part of consensus theory, it has been tacitly assumed that liquidity traps are temporary or “cyclical” problems. But this was not the case in the 1930s and has not been so during the twenty-first century. In both eras, we have suffered from long-lasting (that is, structural) liquidity traps.

U.S. trade deficits measure the gap between the income generated at home and the amount spent on consumption and investment. Without the U.S. government’s deficits, spending demand would have been lower and, unless the trade deficit fell by the same amount, domestic output and employment would have fallen. As the United States had a structural liquidity trap, either the trade deficit had to fall, unemployment had to rise, or the United States had to run a large persistent budget deficit. The decision made in favor of budget deficits was not because they were welcome; rather, the alternatives seemed either unattainable in the case of lower trade deficits, or unbearable in the case of unemployment. It is, however, a policy that is no longer viable, because the rate at which the national debt is rising is much faster than the trend growth rate of national income.

The American Response

The twenty-first century suffers from a repetition of the private sector liquidity trap the global economy experienced in the 1930s. In the 1930s, it could have been alleviated by the Keynesian solution of using government deficits to reduce savings, but today, this has ceased to be a sustainable policy. The liquidity trap is not short-term but structural: fiscal deficits are connected to the large trade deficits which “surplus” countries have been reluctant to relieve, and national debt ratios cannot rise indefinitely. As the problem has become acute and foreigners provide no help, the United States has been forced to act and, in the absence of guidance from sound economic theory, it has chosen the policies of raising tariffs and threatening to impose taxes on foreigners’ U.S. income.

For tariffs to help, they need to cause output to shift from foreign countries to the United States. Trying to judge whether this will be successful can be approached either by assuming that some general equilibrium model can provide the answer, or by attempting a detailed assessment of the impact on different industries and countries.

The second, which is a partial equilibrium approach, strikes me as hopeless. The impact of tariffs fall on one industry, and one country has a knock-on impact on others, and we can’t solve equations which have several unknowns and whose values are not fixed or mutually dependent. It may not be possible to assess the impact of tariff changes on economies but, if it is, we must use a general equilibrium approach, which compares the trade deficit in equilibrium conditions with different tariff levels.

If the deficit is not due to the superior efficiency of foreign production, it follows that the level of the U.S. trade deficit is not due to U.S. inefficiency in particular forms of output but to the excess of imports over exports, which is needed to offset the flow of inward investment. Making the United States a less attractive home for investment will thus alter the level of the current account external deficit, while tariff changes will not. This is not an easily testable conclusion. It follows from the theory of comparative advantage, which has been found robust when tested, but it also requires that exchange rates respond more elastically in the short term than trade flows to changes in international investment preferences. While a reasonable assumption, this is also not a completely testable one, though it has support from the evidence of most usual short-term impacts, which show that trade balances rise rather than fall when currencies weaken. This is known as the J-curve,3 and the “empirical results mostly are supporting the J-curve effect.”4 The initial impact reverses, hence its J-curve name, as trade deficits are not permanently improved by currency appreciation.

“US financial markets are large and open to foreigners. Investors enjoy greater protection than elsewhere. The US courts are more favourable to creditors than those in most other markets.”5 Such was the explanation of the attractions of the United States as a home for other countries’ excess savings published shortly before the new administration took office. The proposed Article 899 of the administration’s “One Big Beautiful Bill” would have given the U.S. Treasury the power to tax foreign companies and individuals on their U.S. income, which “undermines the idea that America is a place of consistent investment laws.”6 Dubbed the “revenge tax,” it was eventually dropped in exchange for concessions from allied economies at the recent G7 summit. Even if not passed, investors will feel less welcome and expectations of the risk of future harm, previously barely considered, will change.

The Problem Remains

While the Trump administration is unlikely to succeed in reducing the trade surplus by its tariff policy, it may well succeed by weakening the dollar; it will then no doubt claim the result as a triumphant vindication for its tariff policy—even if, as seems likely, the J-curve effect results in the short-term combination of a deteriorating trade balance and a lower exchange rate.

Absent any weakening in demand, tariffs push up worldwide prices, which a weak dollar will reinforce for the United States. Experience shows that we are bad at forecasting the main short-term economic variables, and the common escape clause that “Forecasting is particularly difficult today,” has more than usual credibility. Whatever the outcome, it is likely to have been rendered worse by the undermining of trust signaled by threats over tariffs and taxes. Such policies also fail to address the problem, whose causes include China’s approach to the rule of law and surplus countries’ smug contentment with their international balances. Over time, trade deficits may switch between countries, but other changes, such as a major fall in the stock market, will likely be needed for the U.S. trade balance to improve.

So long as the world suffers from its current structural liquidity trap, countries must, in aggregate, run fiscal deficits and, so long as developing economies cannot or do not run trade deficits, the developed ones must run them. As national debt ratios in liberal democracies generally exceed 100 percent of their slowly growing national incomes, ever lower real interest rates are needed to avoid ever rising national debt ratios. Low real interest rates without significant inflation require the lower nominal rates from which we have habitually suffered this century, and which accompany and signal structural liquidity traps. It is, therefore, a rational analysis that has led many to the view that much higher rates of inflation are both likely and required.

The implicit assumption in this analysis is that growth cannot be increased. Fortunately, it can, but the possibility is ignored or denied by consensus economists. Capital inflows are not necessarily damaging, as it is possible to benefit from them, thus substituting a positive advantage for the harm that results from increasing domestic unemployment or pursuing the negative-sum policy of tariffs. Ideas always meet resistance when they upset conventional wisdom, but this one faces the additional problems of requiring an understanding of depreciation and the impact of corporation tax on investment, both of which pose great difficulties for consensus economics.

Trade deficits can be damaging or helpful depending on whether the inflow of capital takes the form of debt or equity—and on what they are used to finance. Subject to important but minor caveats, capital inflows are heavily favorable in either form if they finance business investment, rather than consumption.7 If the inflows are predominantly debt, they will be exceptionally beneficial if they finance business investment and extremely dangerous if they do not. The Greek crisis of 2009 provides a vivid example of the damage done by inflows of debt financing consumption. Had the inflow, which averaged around 10 percent of GDP in the run up to the crisis, financed additional business investment, the taxable capacity of the economy would have risen much faster than interest payments and, while budget mismanagement might still have provoked a crisis, it would neither have been inevitable nor as significant.

The Growth Solution

We have a worldwide structural liquidity trap, which cannot be solved by pushing the trade deficit from one country to another, nor can it be solved just by trying to cut fiscal deficits. Any serious attempt to improve government finances would cause massive unemployment and could easily fail, since tax revenue falls with declining profits and rising unemployment. As these twin deficits cannot be eliminated, they must be accommodated, so the only workable policy solutions are those that use the surplus savings of countries with trade surpluses to finance investment and thereby accelerate the growth of countries with trade and fiscal deficits.

This solution is easy to understand but rarely proposed, and it seems to occur more easily to fund managers than to economists. The failure to propose growth as the answer to our most important economic problem is a symptom of the confusion shown in public debate over both savings and investment. Technological progress is believed to be exceptionally rapid but too slow to stimulate enough investment, and the wish to save is seen as both too high and too low to finance more investment. “[The] ability to fund higher investment is just one necessary condition of faster growth, there must also be opportunities in which to invest . . . growth means change and so requires innovation.”8

There are two common fallacies in the public debate over growth. The first, which is the implicit assumption that private sector savings need to rise to finance growth, is nonsense when the government runs a large budget deficit. Generating more savings is a political and not an economic problem, as it only requires a cut in budget deficits. The economic problem lies in cutting the deficit without creating unemployment, which is solved by more investment. The second fallacy is that opportunities to invest are absent without greater innovation.

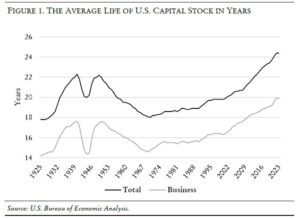

The world is seeking to save more than it wishes to invest. The gap need not be met by lower savings; it can be met by higher investment. Innovation is only needed if existing technology is already being exploited fully. The consensus is happy to rationalize the high investment and growth in emerging economies as the natural result of catch-up modernization, but it assumes, while not pausing to explain why, that this does not apply, even in a weakened form, to all countries less advanced than the United States. Even in the United States, current technology is unlikely to be fully exploited as the average age of business capital is twenty years, and this has risen steadily by 5 percentage points since 1980 (as figure 1 illustrates). The assumption that there is no equipment that can be installed that is not more productive than business capital, which is on average twenty years old, is without evidence and not a sensible claim.

When investment rises, savings also need to rise, but the wish of the private sector to save is the problem, and policy has aimed at thwarting this by a combination of low interest rates, which discourage it, and fiscal deficits, which offset it. These policies will cease to be needed if growth rises, and as cutting deficits seems a sure way of creating unemployment, the aim must be to boost investment without increasing tax or cutting government expenditure.

A change in business behavior is needed, and this requires a change in motivation. “Whatever else may be wrong with economics, its starting point is correct: people do indeed respond to incentives.”9 A corollary of this truism is that the more you tax something, the less you have—and the more you subsidize, the more you get. Cutting the tax that discourages investment and increasing subsidies that boost it should therefore increase investment. If other taxes are raised, the budget deficit need not be changed. As faster growth will follow from higher investment, a reduction in the budget deficit and the high unemployment that will follow will cease to be needed unless there are insufficient savings to finance the additional investment and, if there are, these can be provided by cutting the budget deficit.

Shifting spending from consumption to investment will raise the sustainable level of the world’s fiscal deficit and, if the higher investment is not matched by higher intended private sector savings, it will allow government deficits to be reduced without raising unemployment. Three options are open to policymakers: to do nothing and risk a financial crisis, to cut budget deficits and create high unemployment, or to accelerate growth by changing business incentives.

How Should Policy Change?

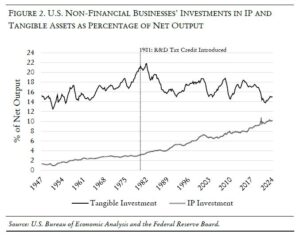

Growth has been slow in the twenty-first century, not only in the United States but in all major developed economies, and this has aggravated the problem of sustained high fiscal deficits.10 Tax credits for expenditure on research and development (R&D) were introduced in 1981. As such expenditure is usually a deductible expense for corporation tax, the credit amounted to a subsidy. Tangible investment has received some similar but only relatively minor encouragement, and depreciation is only allowed over several years, so corporation tax on the profits from tangible investment has remained significant.11

As far as tax and investment subsidies have been used to encourage growth, they have been heavily weighted toward intangible intellectual property (IP) rather than tangible investment, despite the occasional introduction of temporary “full expensing” and other measures, such as those in the latest U.S. tax bill. Since the introduction of the R&D credit in 1981, IP investment has risen from 3 to 9 percent of nonfinancial companies’ net output and tangible investment has fallen from 19 percent to 13 percent (see Figure 2), while the growth rate of the economy has probably slowed since 1975 and the trend has continued this century.12

The policy appears, therefore, to have been very effective in stimulating IP investment and totally unsuccessful in boosting growth, which has presumably been its purpose. Doing the same thing over and over again and expecting different results has been labeled insanity, so a new policy is clearly needed. As the R&D credit has been successful in raising investment in IP but unsuccessful in stimulating growth, a change from subsidizing IP to tangible investment (or simply adding incentives to boost tangible capital) seems like the sensible and pragmatic step to take. There is, however, no apparent pressure to do this, for the following reasons:

(1) It’s a new idea: “The difficulty lies not in the new ideas, but in escaping from the old ones . . . .”13 As Keynes implied, those who teach, while usually quick to learn, are often slow to unlearn the errors they have been taught, particularly if they have also taught them. This is even more prevalent in macroeconomics, where theory has barely changed since the Keynesian revolution.

(2) It is unfashionable: “Technology” has come to be defined as intellectual property alone, to the exclusion of the many physical production inputs required to realize its benefits. The stock market boom has favored IP- and software-based “tech” companies, and this has often led investors and financial journalists to confuse the stock market with the economy and to forget the importance of tangible capital. These commentators often place their hope in some deus ex machina, an unexpected power, with AI as the prime suspect, which will save us from the seemingly hopeless situation presented by fiscal deficits.

(3) Growth benefits labor incomes: it does not, however, increase the return on equity, as numerous studies comparing stock market returns and growth for individual countries have shown.14 Management bonuses are most generally linked, directly or indirectly via share prices, to earnings per share (EPS), and these can rise through buybacks or through tangible investment. Buybacks are less risky, unless competitors are reducing their production costs by investing, so those who run companies dislike rather than applaud incentives for tangible investment.

The dramatic change in management remuneration that occurred in the 1990s and the stock market bubbles have benefited those whose skills lie in finance and intellectual property, rather than in assessing the rewards and risks of tangible investment.15 This has led to opportunities for high returns from more mundane forms of investment being neglected, which has made a major contribution to the rise in the average age of the capital stock (see Figure 2). Incentives that encourage spending on tangible capital are thus likely to have unusually high returns.

Growth Theory

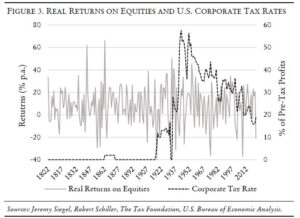

The real return on equities is mean reverting at about 6.7 percent (as shown in figure 3); it is totally unrelated to the effective rate of corporation tax.16 The lack of any connection might be explained in one of two ways: that the level of corporation tax is unrelated to the return, or that the return changes in the same proportion to the change in tax. The second explanation appears to be impossible given the mean reversion of the return on equity, as it requires new investment to be made, despite a rise in corporation tax, in assets whose value is less than their cost. While this can happen through occasional misjudgments, it is not plausible on average over time.

Companies pay corporation tax on their profits after depreciation. As tax does not reduce operating profits, it must reduce depreciation, which fluctuates with several variables that economic policy cannot alter—and with the growth rate of labor productivity.17 Policy decisions, including those which affect the revenue from corporation tax, can only alter depreciation when it results from changes in labor productivity, as the other causes of depreciation are, at least in aggregate, exogenous and thus impervious to policy. Changes in corporation tax thus have a direct impact on depreciation and thereby on growth via labor productivity.

That an economy with a low effective rate of corporation tax will grow faster than one with a higher rate is shown by the exact match, under equilibrium conditions, of changes in the revenue from corporation tax, the level of depreciation, and the growth rate of net domestic product (NDP), which equals the combined income of the economy from wages and profits and equals GDP minus depreciation. NDP also measures the taxable capacity of the economy. The extent by which growth needs to exceed the cost of interest payments on the national debt should be measured using NDP, not GDP; any government that hopes to tax depreciation will be very disappointed.

As the fall in revenue matches the change in the equilibrium growth rate, a cut in corporation tax revenue (CT) will raise the equilibrium growth rate by a matching amount: a cut of 1 percent in CT raises the equilibrium growth rate by one percentage point of NDP. We do not know the economy’s trend growth rate, but we know that it will be increased proportionately by a cut in CT, and we can thereby estimate the reduction needed to make a given level of fiscal deficit sustainable. Cuts in CT must be matched by balancing rises in other taxes; they will otherwise be inflationary. Balanced changes do not involve this risk but will nonetheless accelerate the growth rate of NDP and thereby the level of the fiscal deficit that is sustainable.

The assumption that the real return on equity is mean reverting allows the impact of CT on growth to be known because it is a conclusion which follows from a general, not a partial, equilibrium analysis. It is not, therefore, affected by other variables, such as the level of education, changes in interest rates, or climate change, which may well partly determine the rate of growth by accelerating the speed at which it adjusts to reductions in CT. Thus, altering CT does not allow us to predict the economy’s growth, only the change it will make to it.

Another unknown is the amount of investment and savings that will result from a change in CT. This is because the share of NDP needed to accelerate its trend growth by a given percentage depends on the efficiency of the additions to the tangible capital stock. These additions will be less efficient than those which would have been made had CT not changed. As there are limits to the proportion of NDP that can be saved and thus not consumed, cuts in CT cannot be used to boost growth beyond a certain rate. Advances in technology provide a limit to the growth rate of the economy, but the rate achieved may be well short of the speed that technology makes possible

Keynes showed that “If left to its own devices, the economy [is] capable of operating at below its full potential, not just temporarily, but semi-permanently.”18 Corporation tax has the comparable impact of causing the economy to operate semi-permanently below its full potential growth rate.

Known Unknowns

The rate at which the economy would grow in the absence of any change in the effective rate of corporation tax is not knowable. It depends, among other things, on the rate at which technology improves. AI may cause such a boost to tangible investment and growth that the United States (along with other countries that both have trade and fiscal deficits) can cease to worry as the growth in taxable income outstrips the growth of national debt. But it may not; improvements in computing technology have had underwhelming impacts on growth and productivity in recent decades.

Growth also depends on the negative impact of climate change. The output of hydroelectricity falls as rivers dry up, floods increase the cost of maintenance, and air conditioning becomes essential where it was only a luxury before. There are other unknowns. We are not only ignorant as to how fast we will grow without a change in corporation tax, but our ignorance extends to what has caused growth to fluctuate in the past. So we cannot judge the impact of changes in corporation tax from short-term changes in growth or the level of tangible investment. Public debate is sadly dominated by competing claims for which opposite conclusions can readily be drawn by choosing different periods.

The assumption that the real return on equity is mean reverting allows the impact of CT on growth to be known, however, because it is a conclusion that follows from a general, not a partial, equilibrium analysis. We are lucky to have enough data (223 years of it) to be able to use a general equilibrium approach; partial equilibrium approaches strike me as hopeless not only for assessing the impact of tariff changes but for growth policy. We also know that the effective rate will rise if inflation goes up, though this does not show up in companies’ profits, only in those national accounts in which inflation allowances are made. We don’t know how fast the U.S. economy will grow if the effective rate of corporation tax is unchanged, nor do we know how rapidly cuts in it will boost investment.

But we know that investment and growth will be higher if we cut the effective rate of corporation tax. I am sure that we need faster growth and that relying on AI or good luck to get it would be reckless. So the question, then, is how to go about cutting this rate and boosting investment. Because subsidies depend on investment rising, they cannot be spent on dividends or buybacks. Therefore, I recommend that we cut the effective rate of corporation tax via subsidies specifically targeted at investment, rather than by cuts in the standard rate of corporation tax.

This article originally appeared in American Affairs Volume IX, Number 3 (Fall 2025): 25–38.

Notes

1 This is explained by the Balassa-Samuelson Effect. See: Investopedia Team and Charles Potters, “

Balassa-Samuelson Effect: Overview of the Economic Theory,” Investopedia, September 18, 2023.

2 Paul Blustein, King Dollar. The Past and Future of the World’s Dominant Currency (New Haven: Yale University Press, 2025).

3 The Marshall-Lerner condition states that a change in the exchange rate of a currency will only impact the trade account if the sum of price elasticities of demand for imports and exports is greater than 1.0.

4 Ioannis N. Kallianiotis and Iordanis Petsas, “Trade Deficits and Currency Devaluation: Testing the J-Curve,” International Journal of Business & Management Studies 3, no. 12 (December 2022): 41–64.

5 Kenneth Rogoff, Our Dollar, Your Problem (New Haven: Yale University Press, 2025); the argument is summarized in: Edward Chancellor, “King Dollar’s Shaky Throne,” Times Literary Supplement, May 30, 2025.

6 Gillian Tett, “There’s a Ticking Time Bomb in Trump’s ‘Big, Beautiful Bill,’” Financial Times, May 29, 2025.

7 Inflows that finance housing can be beneficial or neutral depending on their return but, even if debt financed, the benefit is relatively small and, as returns are more volatile than the cost, they are inherently risky.

8 Martin Wolf, “In Tough Times, Good Policy Becomes Even More Important,” Financial Times, April 28, 2025.

9 Martin Wolf, “The Market Can Deliver the Green Transition—Just Not Fast Enough,” Financial Times, November 22, 2022.

10 Robert J. Gordon, “Does the ‘New Economy’ Measure Up to the Great Inventions of the Past?,” Journal of Economic Perspectives 14, no. 4 (Fall 2000): 49–74.

11 The top corporate tax rate in the United States fell from a high of 53 percent in 1942 to a maximum of 38 percent in 1993, which remained in effect until 2018, although corporations in the top bracket were taxed at a rate of 35 percent between 1993 and 2017.

12 Gordon, “Does the ‘New Economy’ Measure Up to the Great Inventions of the Past?”

13 See: “Preface” in John Maynard Keynes, The General Theory of Employment Interest and Money (London: Palgrave Macmillan, 1936).

14 See: “Chapter 16” in Andrew Smithers, The Economics of the Stock Market (Oxford: Oxford University Press, 2022).

15 Andrew Smithers, Productivity and the Bonus Culture (Oxford: Oxford University Press, 2019).

16 The effective rate of corporation tax is the ratio of tax paid, net of any investment credits, as a percentage of profits before tax. It is thus a matter of indifference whether alterations in the effective rate arise from changes in subsidies, or headline tax rates, or through fluctuations in inflation.

17 R.M. Solow, J. Tobin, C.C. von Weizsacker, and M. Yaari, “Neoclassical Growth with Fixed Factor Proportions,” Review of Economic Studies 33, no. 2 (April 1966): 79–115.

18 Tim Lankester, Inside Thatcher’s Monetarism Experiment (Bristol: Bristol University Press, 2024).