The economic performance of the United States and other major developed economies in the twenty-first century has been appalling, whether in comparison to the period of nearly eighty years since World War II or with the rest of the world over the past two decades. Having suffered the most severe postwar financial crisis in 2008, we now face a high risk of another one; real output and incomes have stagnated and inflation has shot up. This abject failure has dangerously damaged liberal democracy. Voters are angry and faith in experts has fallen.

Central bankers have been blown off course by Covid and the Ukraine war. But while the pandemic and Putin’s invasion have been damaging, they are only a small part of the problem. The stagnation of income goes back to the beginning of the new century and the upsurge in inflation was under way well before Russia launched its attack. So, even allowing for bad luck, policy errors have made a major contribution to our current malaise. This may not, however, indicate operational incompetence by governments and central bankers. Policy is necessarily based on theory, so mistakes can arise either from poor judgment in applying a sound theory or from the inevitable failures of implementing a bad one.

In the eighteenth century, doctors were probably more deadly than disease. This was not because doctors were incompetent; it was because they had been taught nonsense. Similarly, the disastrous start to the twenty-first century follows from the errors of economic theory rather than from mistakes in its application.

Like eighteenth-century medicine, the economics of today is basically unscientific: it is incompatible with the evidence. Until current theory is replaced, we will continue to suffer from stagnation and regular financial crises. Better theory is, however, available and, if used, would provide the tools we need for a well-managed economy, in which growth will replace stagnation amid low and broadly stable levels of unemployment and inflation.

Three Equilibria

Consensus macroeconomics rests on two assumptions. The first, which is termed profit maximization, is that companies invest with the aim of maximizing the value of their net worth. The second is that this is done by investing when returns compare favorably with the cost of capital, which varies with real short-term interest rates. From these assumptions it follows that we live in an economy whose stability can be maintained as long as demand matches the supply available. In the words of Ricardo Caballero, consensus theory holds that we have a one-deviation-at-a-time economy.1 But these assumptions are wrong and, as a result, so are the consequent conclusions. We live in a world where there are at least three equilibria which must be maintained for economic stability. In addition to balancing demand, we must avoid excessive levels of both asset prices and money supply.

Three problems require three solutions, and the solution to one must not create another disequilibrium. In other words, if demand is weak, we must have a way of boosting it without pushing up either asset prices or money supply. We must therefore understand the policies needed to keep each equilibrium independently in balance.

At any time, there is an equilibrium rate of unemployment consistent with a stable rate of inflation; this is the non-accelerating level of unemployment (nairu), which is constant unless there is a change in expectations about inflation. In the absence of such changes, inflation and unemployment will be stable if demand changes at the same rate as potential output, which is the trend growth rate. The twin tasks of demand management are thus to avoid demand growing either faster or slower than trend, and for this to take place at a low and stable level of inflation, so that inflationary expectations do not rise.

It used to be assumed that demand could be kept in balance by changes in short-term interest rates, but Keynes showed that demand did not always rise and fall to match rate changes. In these conditions, known as a liquidity trap, intentions to save exceed those to invest, and unemployment will rise unless there is a boost to demand. When monetary policy ceases to be effective, another source of demand is needed, and for this Keynes proposed changing the government’s budget deficit (fiscal policy). When government spending rises more than its income, the government’s savings fall, and this reduces the economy’s total savings. In neo-Keynesian terminology, changes in budget surpluses and deficits enable an ex ante surplus of savings over investment to be brought back to zero without the need for any rise in unemployment.

Keynes assumed that liquidity traps would be temporary affairs resulting from short-term falls in investment in response to the ebb and flow of business optimism. He therefore ascribed temporary weakness in business investment to a decline in “the animal spirits of entrepreneurs.” But our experience this century is not only for such temporary losses of confidence, as occurred after the financial crisis of 2008, but a longer-lasting tendency for investment to be insufficient to match the desired level of savings. We thus have an economy with positive net ex ante savings, which tends to be structural. It is difficult to combat such a situation with persistently high levels of budget deficits, which can lead to an ever-rising ratio of government debt relative to GDP. This becomes particularly threatening when, as so far this century, trend growth is near zero.

A liquidity trap which appears to be long-lasting rather than cyclical presents central banks with a major dilemma. Their attempted solution has been to try and boost demand by buying long-dated bonds through quantitative easing (QE), which has depressed their yield relative to short-term interest rates—flattening the yield curve. In terms of supporting demand, the policy has been successful. By preventing excess net ex ante savings, central banks have been able to maintain demand at the trend level of output. Had the consensus model been correct, this would have produced economic stability. But it isn’t, and therefore, it hasn’t. QE has destabilized the other equilibria needed for stability. It has produced excessive levels of both asset prices and money supply.

Fiscal policy is the appropriate instrument to offset short-term cyclical declines in demand but not for prolonged liquidity traps. We therefore need another policy instrument to ensure that short-term interest rates do not fall to levels at which they cannot on their own be used to control demand.

For short periods, declines in short-term interest rates boost equity prices, but the effect falls off quicky and is virtually nonexistent over five years.2 Such changes have a much smaller impact on the value of corporate assets, so declines in short-term interest rates have the temporary effect of pushing up share prices more than net worth; q (which is the ratio of the stock market value of companies to their net worth) therefore rises. But q is mean reverting,3 so the stock market will tend to fall back unless short-term interest rates keep declining, and the fall will be enhanced by the degree to which q is above its mean reverting average. The strength of q’s mean reversion is like that of an elastic band: the more it is stretched, the stronger is the force bringing it back and the faster the change is likely to be.4 A sharply falling stock market thus becomes more likely at higher levels of q, and the likelihood of sharp declines is even more probable if they are reinforced by rising short-term interest rates.

It is therefore dangerous to boost demand by reducing short-term interest rates unless q is near or below average. As q rises when interest rates fall, using cuts in interest rates to maintain ex ante net savings at zero ignores the risks of one disequilibrium while seeking to balance another. This would be impossible if the consensus model were correct, as there would only be one disequilibrium to worry about. Unfortunately, the model is wrong.

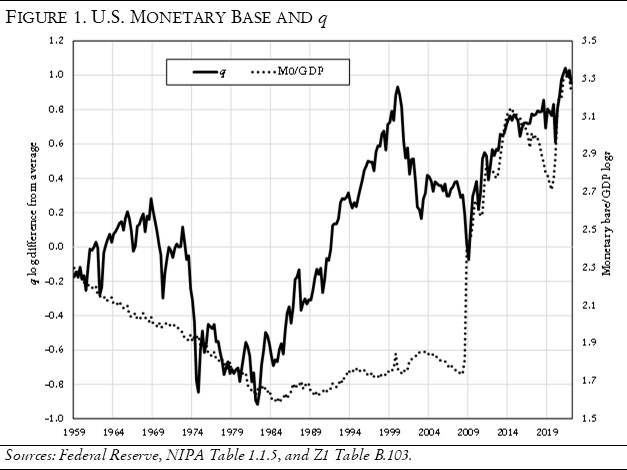

Cutting interest rates can lead to financial crises. QE involves central banks buying long-dated bonds and this naturally pushes up their prices and reduces their yields. Share prices respond to long-term as well as short-term interest rates, so q is pushed up by QE. When central banks buy bonds, the sellers’ holdings of cash rise. If the sellers are banks, this shows up in their holdings of deposits with the central bank. In the United States, QE has caused a massive rise in the ratio of such deposits with the Federal Reserve. These deposits are the main constituent of “base money” (M0). QE has thus caused the ratio of the monetary base to GDP to rise to levels which are way above any previously seen.

Cutting short-term interest rates is dangerous when q is above average, and the danger is enhanced if such cuts are accompanied by QE. This is illustrated in figure 1, which shows that the ratio of the monetary base to GDP fell from 1950 to 1984, at a time when q declined, rose slowly to the year 2000, and then shot up from 2009. As q responds to short-term interest rates as well as changes in the M0/GDP ratio, the two ratios do not move exactly together, but the influence of QE on the overvaluation of q fits neatly with figure 1. The decline in q from 1950 to 1984 was accompanied both by rising interest rates and a fall in the ratio of the monetary base to GDP. The rise in q from 1984 to 2000 was a period in which interest rates fell sharply and q rose. The post-2000 fall in the stock market was halted in 2009 at a time when M0/GDP rose at a record-breaking pace and both ratios have since risen to record-high levels.

James Mitchell has shown that share prices respond to profits as well as interest rates,5 so I am not suggesting that the stock market’s level could be predicted solely from accurate forecasts of interest rates and the monetary base, even if such forecasts were possible. But current policy calls for the Fed’s holding of government debt to be run down. This will produce a fall in the monetary base, which seems likely to have an important and negative impact on U.S. share prices.

Considered from the viewpoint of economic policy, the use of QE to boost demand at a time when it is unresponsive to short-term interest rates is extremely dangerous if q is elevated. The danger of using QE applies also to funding policy, which depends on whether governments choose to borrow by issuing long-dated bonds or short-term Treasury Bills. Funding policy can thus have the same effect on bond yields as QE and should be avoided for the same reasons.

People judge their wealth largely from the level of share prices, so when q is high, they overestimate their long-term prosperity. Their apparent need to save therefore falls as the value of q increases. Share prices decline more rapidly than they rise, and this tendency is enhanced to the extent by which q is above average. The economy is thus vulnerable to falls in the stock market and particularly to rapid declines, which have a marked effect on both households and companies. Savings rise as people seem poorer and experience justifies their worries that a weak stock market is often followed by rising unemployment. These concerns also affect business confidence, so the animal spirits of entrepreneurs weaken. Companies become cautious about borrowing and investing. Lenders become nervous about providing finance, and companies worry that additional debt may not be available if needed.

Sharp falls in the stock market thus regularly result in sharp rises in ex ante net savings, so that a boost to demand becomes necessary to stop unemployment rising. If q is above average, it will be dangerous to cut short-term interest rates. It is then better to use fiscal rather than monetary policy to stimulate demand. But neither response is satisfactory if the tendency for ex ante net savings to be positive is a structural rather than a temporary cyclical problem. Boosting demand with low interest rates and QE drives up private sector debt as well as q and makes financial crises likely; using fiscal stimulus to solve a long-term problem raises the specter of an ever-rising ratio of debt to national income. As neither fiscal nor monetary policy are suitable instruments to deal with a structural tendency for ex ante net savings to be positive, these conditions, which have predominated this century, require an additional policy tool to boost demand. When fiscal policy ceases to be politically possible or even sensible, when q is at or above average, and demand then threatens to be insufficient to maintain unemployment at the nairu, a third policy instrument is essential.

Stable Levels of Money Supply

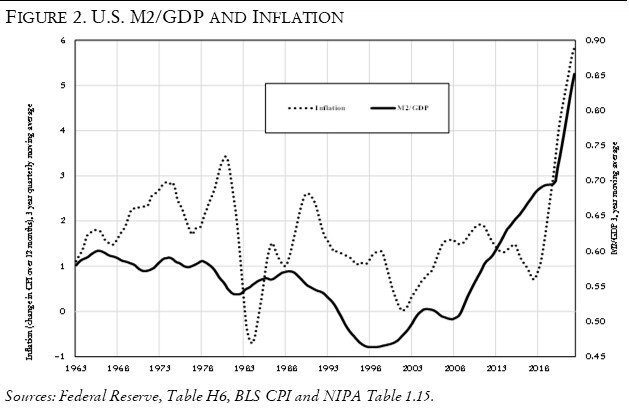

The relationship between money supply and inflation is, to put it mildly, controversial. It is generally recognized that a large jump in the ratio of money supply to output is typically followed by a marked rise in inflation, but attention to monetary data has become unfashionable in recent years because their fluctuations have appeared to have been of no practical importance. As figure 2 illustrates, the ratio of money to GDP fluctuated between 1963 and 2013 without any apparent relationship with the rate of inflation. It was only in 2013 that the ratio moved above its post-1963 level. It then increased sharply, followed by inflation rising sharply from 2019 onwards.

As a paper in the Scandinavian Journal of Economics concludes, central bankers and economists generally appear to have made a serious error by ignoring the data on money supply.6 When inflation is low, it seems that “the link between money and inflation is weak or absent.”7 The practical conclusion is that short-term fluctuations in the ratio of money supply to GDP provide no useful guide to demand or inflation, but that a large rise in the ratio must be avoided. Jumps in money supply do not necessarily signal that current demand has become too strong to allow inflation to be stable. Inflation seems to respond quickly to excess demand, but in the words attributed to Milton Friedman, its relationship with money supply has lags “which are long and variable.” The disequilibrium that arises from excessive growth of the money supply has a different timescale from that caused by excess demand.

We thus have three possible disequilibria in the economy. Demand must be controlled so that unemployment is at its non-accelerating level (nairu), and neither q nor the ratio of money supply to GDP must be allowed to become elevated. Short-term fluctuations in the ratios of q and money supply to GDP do not, however, appear to cause problems and can be treated in statistical terms as “noise” rather than “signal.” But, as we have three disequilibria that must be maintained for economic stability, we cannot successfully manage the economy with only the two currently available instruments of fiscal and monetary policy.

Tax Policy as a Third Tool

Demand needs to be boosted when ex ante net savings threaten to exceed zero, and unless the problem is a short-term cyclical one, neither monetary nor fiscal policy provide viable solutions to it. Monetary policy will not be suitable if q is elevated, and fiscal policy will be equally inadvisable if it threatens to result in an ever-rising ratio of national debt to GDP. These are the conditions that we have experienced this century, and which have been termed secular stagnation. From the viewpoint of economic policy, they are best described as a liquidity trap which is structural rather than cyclical—this highlights the fundamental nature of the problem. It is structural rather than short-term when intentions to save threaten to be greater than those to invest for so many years that attempts to avoid the trap through monetary policy is inappropriate, not only because it causes unstable levels of asset prices, but also because prolonged low levels of interest rates tend to result in dangerously high levels of private sector debt. Seeking to avoid a prolonged liquidity trap by fiscal policy offers the prospect of an indefinite rise in the ratio of national debt to GDP. This rightly raises political obstacles and can cause a collapse in both bond and foreign exchange markets, as the UK showed when a large fiscal stimulus was proposed by Liz Truss, and the market reaction cut short her stay as prime minister to only fifty days—the briefest on record. Among other characteristics, the third policy tool thus needs to be one which avoids driving up debt ratios in either the public or private sectors to levels which financial markets consider to be unsustainable.

Tax policy is available for this role. There may be other tools as well, but I know of no other concrete suggestions. Tax policy is not the same as fiscal policy, as it involves no change in the government’s budget deficit. It consists in raising tax revenue from one source and cutting it from another. To be effective, the tax cut must stimulate investment and the tax rise should reduce, or at least not increase, savings. If these twin aims can be achieved, then investment intentions will rise more than those to save, thus giving the required boost to demand.

Corporation tax provides revenue to the government, which must be paid by someone, and the taxpayer will have less money to spend elsewhere. Corporation tax could be passed onto shareholders, or to incomes from employment, or fall on companies’ own spending which, as they don’t consume, must be investment.

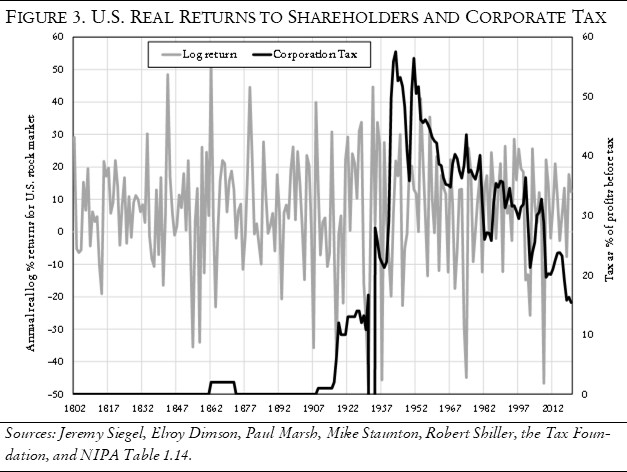

Figure 3 shows that corporation tax cannot fall on shareholders. If it did, shareholders would be worse off and receive lower returns on their shareholdings when corporation tax is high. But, as the chart shows, real shareholder returns have rotated around a stable average of about 6.6 percent, and this has been the same whether there was no corporation tax, as was the case for most of the nineteenth century, or since 1917, when it has always been significant, subject only to the amount of profits that could be taxed. The lack of pain for shareholders is also shown by the fluctuations of returns over the past century, which have been totally unrelated to the current rate of corporation tax. Yet no tax can be levied without hurting someone or something.

Shareholders might have avoided corporation tax by simply passing its burden onto consumers by leaving wages unchanged. If this has occurred, then profit margins would have had to rise, and employees’ share of output would have fallen. But we have data on the division between profits and employment, which together amount to 100 percent of output. As figure 4 shows, there has been no connection.

Corporation tax thus has no negative impact on the incomes of shareholders or employees. It therefore cannot fall on the amount that either group has available to spend on consumption. Hence it must fall on private sector investment.

Cutting the revenue from corporation tax will thus increase the level of investment above what it otherwise would be. As there are many other things which affect how much companies will invest, its level also changes independently of any variation in corporation tax revenue. We cannot therefore expect investment to rise and fall each year in line with its changes. But we can see the effect of corporation tax if we look at longer term data and, as illustrated in figure 4, we know that investment will be greater than it would have been if the tax revenue from corporation tax is reduced.

Tax policy, as distinct from fiscal policy, requires that the government’s budget deficit does not change. The fall in revenue from corporation tax must therefore be matched by a rise in revenue from a tax that hits consumption, not investment. Whichever way taxes on consumption are raised, they always reduce people’s spendable income. When incomes fall, households seek to reduce their consumption by as little as possible and do not respond by increasing their savings. The level of household savings does not rise and may well fall with increased taxes on consumption. The combination of reduced revenue from corporation tax and higher taxes on consumption thus boosts business investment without increasing household savings. Although corporate savings tend to rise with capital spending,8 the net effect is to raise spending more than savings, stimulating total demand as well as shifting it from consumption to investment.

Tax policy is needed to avoid the problem of our current prolonged liquidity trap, as attempts to use monetary or fiscal policy to do so have resulted in today’s multifarious problems. Tax policy carries with it the prospect of a double benefit in that it should not only free us from policies which have resulted in rapid inflation and a high risk of another financial crisis, but also free us from the longer-term problem of low trend growth with which the twenty-first century has so far been cursed.

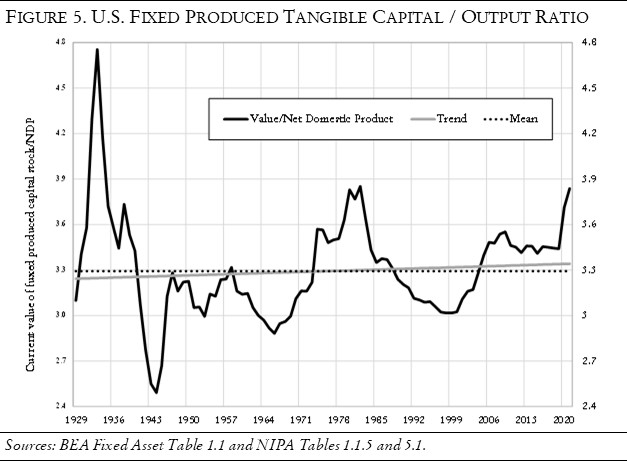

The capital stock of the economy consists of buildings, equipment, inventories, natural resources, and land. We cannot add to the last two, which are natural endowments and, while inventories are necessary, the need for them rises in line with output. We can, however, add to our stock of buildings and equipment, which is the amount of “fixed produced tangible capital.” As figure 5 illustrates, there is a stable and probably mean-reverting ratio between the level of this capital and that of output.9 If we boost the rate at which such capital expands, we will also speed up the rate at which output grows. To do this, we need only increase the ratio of tangible fixed capital investment and, if this is accomplished, we will also increase the trend growth rate of the economy. Spending on intellectual property (IP) is much less effective in boosting growth than money spent on tangible capital, because trend growth moves in line with the value of the stock of capital and IP is depreciated over four times faster that tangible capital.10

Optimizing the Incentive to Invest

“Whatever else may be wrong with economics, its starting point is correct: people do indeed respond to incentives,” writes Martin Wolf.11 A corollary of this truism is that the more you tax something, the less you have, and the more you subsidize, the more you get.

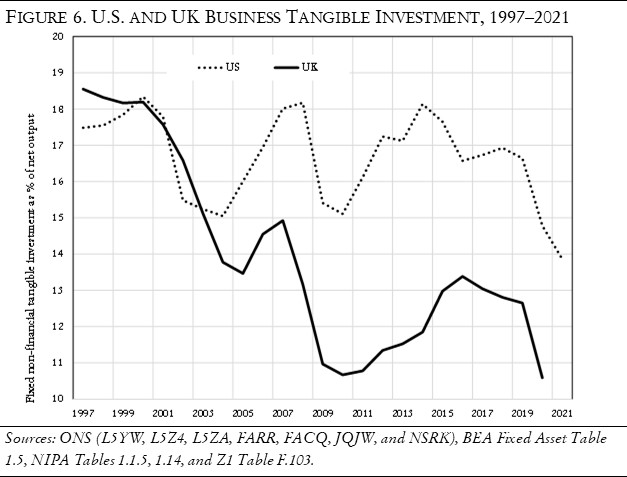

A key principle of sound tax policy is to achieve as much beneficial change as is possible from the smallest degree to which tax rates are altered. The revenue from corporation tax can be lowered either by reducing the headline rate or by giving subsidies in proportion to the amount invested. Given the choice between subsidies which encourage investment and cutting corporation tax to reduce the disincentive to it, we should prefer positive incentives. The boost will be most effective if it causes a rise in earnings per share (EPS), because the weakness in investment this century, which is illustrated in figure 6, has been caused in part by the way business managers have been paid in recent decades. The 1990s saw a huge increase in the pay of senior executives, mainly via bonuses. This shifted the balance between the two major concerns of senior executives, which are to keep their jobs and to be highly paid.

Jobs are at risk if companies invest either too much or too little. Shareholders like rising EPS, which investment tends to reduce, as the benefits it brings are often delayed until sales have risen, while its costs, including more depreciation, are more immediate. But investment is also essential for improving productivity and, unless it advances, companies risk having higher production costs than their competitors. They then risk losing their market share as their competitors’ lower costs allow them to spend more on marketing or reduce their prices. Once companies start to lose market share, their survival is at risk.

The PE multiple, which is the ratio of share price to profits per share (EPS) is the single most important criteria used for share evaluation. As share prices are heavily dependent on EPS, bonuses are usually linked to them either directly or via total shareholder returns (TSR). The arrival of the bonus culture thus increased the benefits to managers of a rise in EPS and shifted the degree of importance placed on being highly paid in the short term compared to the longer-term goal of keeping the job. Short-term rewards became more valuable and reduced the pain of being dismissed. The weakness of capital spending by business this century is thus partly due to the dramatic arrival of the bonus culture in the previous decade.12 On the other hand, subsidies to companies which result in increases in EPS will shift the impact of the bonus culture from inhibiting investment to encouraging it.

The return on capital is equally unaffected either by cuts in the rate of corporation tax or subsidies for investment, but their impact on the EPS of individual companies will differ. Subsidies will raise EPS more for those who increase their level of investment than those who don’t, while this incentive is absent when the overall rate of corporation tax is changed. Subsidies are thus likely to raise investment by more than the same loss of tax revenue from a cut in the rate, particularly if the accounting treatment is favorable. Bonuses tend to move with EPS, and the extent to which they will rise thus depends on the way they are measured.13 The accounting system used is therefore important and this is likely to be different if the incentive takes the form of accelerated depreciation or is a cash credit proportionate to the amount of the investment. A credit leaves future depreciation allowances unchanged, whereas they decline when they are accelerated. The improvement in this year’s EPS will be smaller if allowance is made in the accounts for the higher future tax payments that will result from lower future depreciation. Subsidies for investment should not therefore result in any reduction in future tax and should not take the form of accelerated depreciation but be cash amounts paid as a proportion of investment.

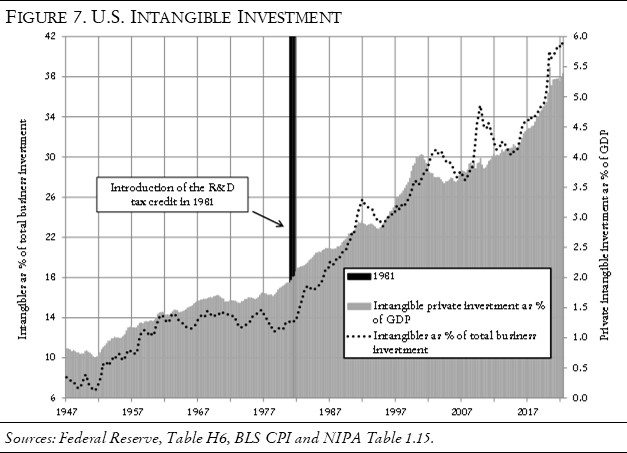

The importance that incentives can have on stimulating tangible investment is illustrated by their powerful impact on intangible spending (IP). As figure 7 illustrates, from 1961 to 1981 U.S. business investment in intangibles fell slightly as a percentage of total investment, but following the introduction of the tax credit for research and development (R&D) introduced in 1981, it has risen from 13.7 to 41.4 percent of business investment and from 2.0 to 5.4 percent of GDP.

As R&D expenditure is fully allowed as a deduction for corporation tax, the accounting treatment resulting from the tax credit brings an immediate benefit to EPS, and figure 6 illustrates how effective it has been for IP investment. The sharpness of the rise in R&D in response to the subsidy raises the reasonable expectation that one for tangible investment would also have a sharply positive impact on the growth of the capital stock and output. This is, however, subject to three important provisos: (1) The effect would not be offset by other negative factors affecting investment, such as weak demand, or rising inflation with its resulting increase in the effective rate of corporation tax. (2) The credit is seen as a long-term policy change, since tangible investment takes time first to plan and then to implement. (3) The accounting treatment should be favorable and lead to a rise in earnings per share (EPS). The greater the increase in EPS, the larger will be the rise in investment.

Folly and Inertia

In addition to the way tangible business investment is taxed or subsidized, its level depends on many things including the way technology advances, the disincentives of the bonus culture, and expectations—the animal spirits of entrepreneurs—over which governments have little if any influence. All we know is that investment will be higher than it would otherwise have been if it is subsidized not taxed. As we need more investment to avoid inflation and financial crises, we have been foolish to tax investment and should now subsidize it. We have been foolish because corporation tax does not reduce our current consumption, only our future prosperity, and because it is widely and wrongly believed to be paid by shareholders. Both these follies follow from the consensus economics ignoring the data on the return on equity, which is ignored because it proves the consensus model is wrong.

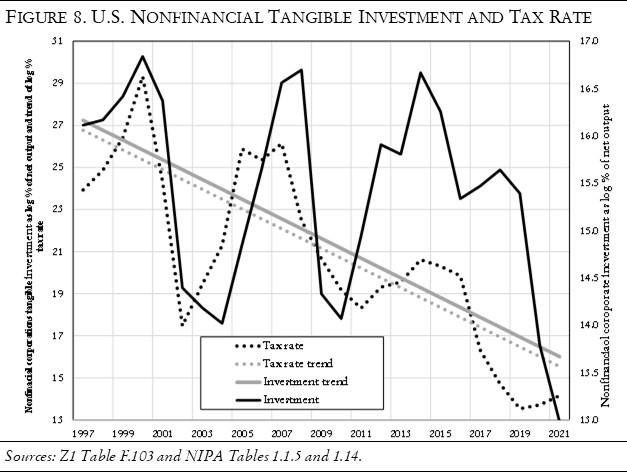

Figure 8 shows that this century has seen declines in business investment and in the effective rate of corporation tax.14 It also shows that the trend of the decline in each case has been very similar, as have the swings from year to year. This does not prove that the decline in the tax rate has boosted business investment above the level it would otherwise have been, but it is consistent with such an assumption. This conclusion is confirmed by the data set out in figure 6, which shows that investment has held up in the United States more than it has in the United Kingdom, where, due to the abolition of ACT, the rate of corporation tax has risen since 1997.

To jump-start investment today probably requires a greater immediate incentive than will subsequently be required to maintain the improvement, because the bonus culture has reduced the incentive to invest not only by increasing the short-term reward for increasing EPS but by reducing the risk that competitors will raise their spending on tangible capital. As I wrote in an earlier piece, “Before 2000, companies increased investment in response to corporate tax cuts, but afterwards, they stopped doing so.”15 The bonus culture is possibly the most important reason for the low level of tangible investment this century. The use of specific investment tax credits will reverse the impact of bonuses from inhibiting to encouraging capital spending, and we should make the initial change particularly strong by making managements fearful that their competitors will be increasing their level of investment. Corporation tax receipts are currently running at about 1.2 percent, and tangible business investment at 7.2 percent of U.S. GDP, so a 20 percent credit for tangible investment would offset the current revenue from this ill-considered tax which falls on investment. It would amount to a positive net subsidy if, as seems probable, investment rises as the economy recovers and should provide the kick-start needed to overcome two decades of inertia.

Despite the urgent need for more business investment, tax changes proposed in both the United Kingdom and the United States will depress it to a lower level than it would otherwise be. The associated failure to use tax policy as a tool of economic management will also make it more difficult to avoid inflation and financial crises. The folly of government policy is due to a poor understanding of economics and is therefore unlikely to change until the current consensus model is scrapped and replaced.

This article originally appeared in American Affairs Volume VII, Number 2 (Summer 2023): 33–49.

Notes

1 Ricardo J. Caballero, “Macroeconomics after the Crisis,”

Journal of Economic Perspectives 24, no. 4 (Fall 2010): 85–102.

2 James Mitchell, “Interest Rates, Profits and Share Prices,” Wall Street Revalued: Imperfect Markets and Inept Central Bankers, by Andrew Smithers (Chichester, UK: John Wiley & Sons Ltd., 2009), Appendix 3.

3 Andrew Smithers, The Economics of the Stock Market (Oxford: Oxford University Press, 2022).

4 There is an analogy in physics where the strong nuclear force has the same characteristic.

5 Mitchell, “Interest Rates, Profits and Share Prices.”

6 Francesco Papadia and Leonardo Cadamuro, “Successful Central Banks Can Afford to Pay Scant Attention to Money,” forthcoming.

7 Paul De Grauwe and Magdalena Polan, “Is Inflation Always and Everywhere a Monetary Phenomenon?,” Scandinavian Journal of Economics 107, no. 2 (June 2005): 239–59.

8 The evidence for this is set out in chapter four of The Economics of The Stock Market and illustrated in figures 6 and 7.

9 The closeness of the average to the trend shown in figure 5 provides an indication of the probability of the ratio being stationary. The depression of output caused by Covid in 2021 will have increased the trend of the ratio, even though this is measured over ninety-two years.

10 Several papers have been published which claim that IP should be depreciated more slowly, but I have shown that the opposite is true and the BEA should depreciate IP even more rapidly. Andrew Smithers, “The Debate over Intangible Capital,” World Economics 21, no. 1 (January–March 2020): 11–38.

11 Martin Wolf, “The Market Can Deliver the Green Transition—Just Not Fast Enough,” Financial Times, November 22, 2022.

12 For a more detailed explanation see Andrew Smithers, Productivity and the Bonus Culture (Oxford: Oxford University Press, 2019).

13 Accounting treatment does not necessarily accord with “real changes,” but reality responds to accounting treatment if linked to pay, which is undoubtedly real.

14 I have used log percentages so that the proportionate changes in tax and investment are more easily compared visually.

15 Andrew Smithers, “Savings Glut or Investment Dearth,” American Affairs 4, no. 4 (Winter 2020): 36–45.