“He became fascinated by the contortions of money—how it could be made to bend back upon itself to be force-fed its own body.”

—Hernan Diaz, Trust

Sea changes in financial markets are not always obvious. It is now undeniable that open-market share buybacks have had a significant impact on equity markets, but little was made of the adoption of the SEC’s 10b-18 rule in 1982, which allowed corporate share repurchases to eventually become widespread.1

The evolving annuity market, still relatively small, may represent another such transformation. The rapidly blossoming marriage of private credit and insurance retirement liabilities contorts the economic identity that investment is a function of savings. Amid these changes, private equity firms found a long-horizon capital source in life insurers, whose annuity and pension liabilities require consistent, bond-like returns. These private equity–owned insurers invest in private credit, which in turn funds further “esoteric” or asset-backed loans. The result is a circular system wherein retirement savings feed insurance contracts, which fund leveraged private lending, which then loops back to support the insurers’ spreads and payouts. This feedback loop has shifted capital allocation from equity-based entrepreneurial ventures to debt-focused strategies, potentially constraining long-term growth in favor of structured finance.

Delivering Retirement versus Allocating Capital

Financial markets, ostensibly the mechanism for allocating capital to productive enterprises, have come to be viewed by investors, policymakers, and the public as vehicles for funding retirement.2 This shift is not merely one of perception. Policies designed to shore up financial markets and protect investors following the 2008 financial crisis, such as the Department of Labor’s updated Fiduciary Rule and the banking reforms instituted by Dodd-Frank, reshaped both savings and lending. By reducing the margins of the traditional asset management business and creating an advantage for non-bank lenders in debt capital markets, they contributed to the growth of passive, low-cost investing and ignited the market for so-called private credit. These independent, largely unrelated trends have reconverged in the market for retirement assets.

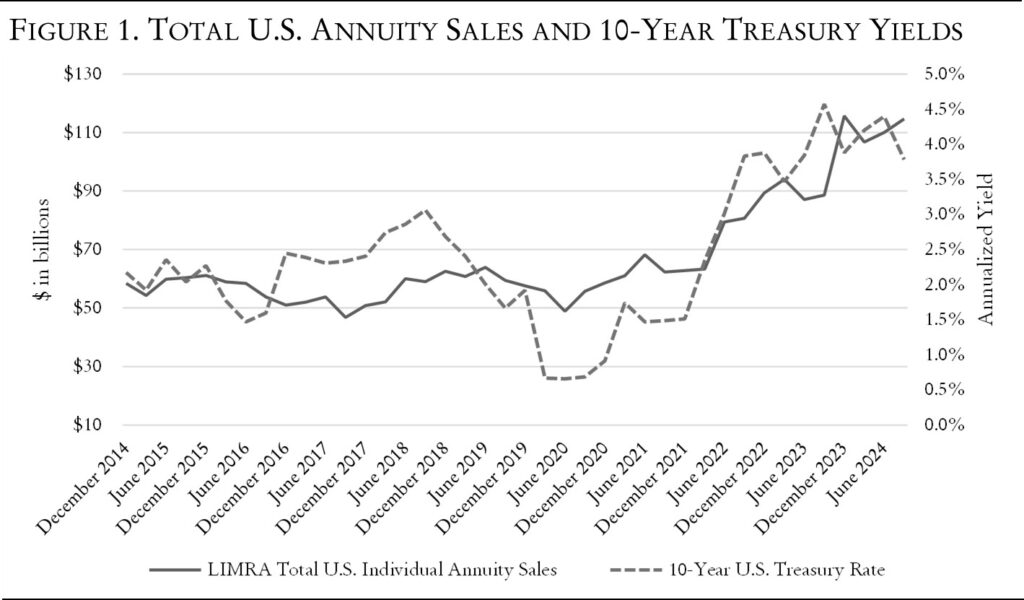

In the drama of global finance, retirement savings play a minor but influential role. At the end of 2022, there were $40 trillion of retirement assets, with $27 trillion being held in public or private investment funds.3 According to research by J.P. Morgan, 72 percent of savers cite saving for retirement as their primary financial goal. Overall, the last decade and a half has been kind to savers as crises, both real and perceived, pushed interest rates lower and raised the value of all financial assets. With rates now rising, the starting valuations of most financial assets make the math of delivering retirement outcomes via traditional investing more questionable. Thus, the once staid annuity market has a renewed appeal for future retirees and new relevance as a growth driver for asset managers.

Annuities are insurance contracts wherein an investor makes a one-time purchase (or series of purchases) in return for a regular monthly payment beginning at a specified date in the future. These come in various structures, with either fixed or variable payments tied to index performance. Higher rates, extended equity valuations, and greater perceived financial volatility have resulted in record growth for the annuity industry. According to limra, an industry group focused on the insurance industry, 2023 annuity sales reached an all-time high of $385.4 billion, while preliminary numbers suggest 2024 sales will come in even higher.4

Like other forms of insurance, the annuities business aims to profit from the spread between the promised payouts and the return on invested assets. Increasingly, that spread comes from debt originating in the non-bank lending market, to which insurers and their large pools of capital have greater access.

In the United States, retirement has often found itself at the center of financial twilights. The gradual decline of defined-benefit pension plans coincided with a general trend toward more informal employment; the rise of defined-contribution retirement plans correlated with the rapid growth of financial services; and now the resurgence of annuities provides feedstock for exponential credit creation. The changing nature of retirement charts the long course of American corporate history and highlights the degree to which the economy has become reliant on debt as a means of extracting higher nominal returns from an economy struggling to generate real ones.

From Company Pensions to Passive Investing

In 1963, the Studebaker Corporation collapsed and took its pension with it. The impact on workers was devastating and highly uneven. The plan’s structure dictated that retirees and workers over age sixty receive their full pensions. Younger workers, however, received only about 15 percent of their earned benefits in a lump sum payment, while those under forty—regardless of their years of service—received nothing. This stark disparity highlighted the precarious nature of pension promises and the need for reform.

The United Autoworkers Union (UAW), which had become interested in developing ideas for pension insurance after earlier failures at companies such as Packard, recognized the Studebaker shutdown as a perfect “focusing event” to promote pension reform. Working with Senator Vance Hartke of Indiana, the union helped draft the “Federal Reinsurance of Private Pensions Act” in 1964, an attempt to create some form of protection from loss of pension benefits.5 Ultimately, the bill didn’t pass, but it was significant in introducing the concept of federal pension insurance into policy discussions for the first time.

Over the next decade, the Studebaker case became a powerful symbol repeatedly invoked by pension reform advocates. The incident illustrated that voluntary pension promises, without federal oversight or insurance, left workers vulnerable to losing their retirement security. Sustained advocacy eventually led to the Employee Retirement Income Security Act (erisa) of 1974, signed into law by President Gerald Ford.

Crucially, erisa put retirement under the shared purview of the Department of Labor and the Internal Revenue Service. Company-sponsored defined-benefit pension plans were overwhelmingly the standard vehicle for retirement savings. At the time of erisa’s passage, defined-benefit plans had 27.2 million active participants versus 11.2 million active participants in defined-contribution plans.6 In a defined-benefit plan, the employer bears the full costs of the retirement benefits and takes on the investment risk using actuarial assumptions about their workforce to arrive at a pension liability (or asset) carried on the balance sheet.

Erisa created two major protections for retirement benefits: pension insurance and fiduciary obligations. The law established the Pension Benefit Guaranty Corporation (PBGC) to insure defined-benefit pensions, directly responding to failures like Studebaker. This insurance program guaranteed basic pension benefits even if an employer’s plan failed.

Alongside insurance, erisa established strict fiduciary duties for those managing retirement plans, which were also extended to all providers of investment management or advice. Initially implemented through a 1975 rule, the Fiduciary Rule was a five-part test governing investment advice. All criteria had to be met: making regular recommendations, having mutual understanding with clients, providing a primary basis for decisions, and offering individualized advice. In sum, the rule mandated that those deemed fiduciaries act in the best interest of their clients. Professor of law and former SEC director William Birdthistle writes, “[i]n the dusty tomes of Anglo-American jurisprudence, the status of fiduciary carries with it rhetoric requiring almost religious self-sacrifice.”7 The key language in the law includes “defraying reasonable expenses of administering the plan” and “with the care, skill, prudence, and diligence under the circumstances then prevailing that a prudent man acting in a like capacity and familiar with such matters would use in the conduct of an enterprise of a like character and with like aims.”8

Absent a reliable ex-ante test for determining investment prudence, fees became the locus of adherence to the standard. This had significant implications for the investment management business. Price, as defined by fees, became the primary theater of competition among asset management firms. Passive strategies that aim to track an underlying benchmark became the default investment choice across retirement savings vehicles. These funds have the lowest expense ratios and, as a result, saw their assets under management explode as defined contributions and self-directed retirement vehicles came into prominence. As of November 2024, passive investing makes up over 50 percent of global equity mutual funds and ETFs.9

The 2006 Pension Protection Act further spurred growth in passive assets. The Act marked a pivotal shift in retirement planning by establishing the Qualified Default Investment Alternative (QDIA) framework within defined-contribution plans. This change came as part of a broader transformation from traditional defined-benefit pension plans to employee-directed 401(k)s and similar accounts.

The Act’s QDIA provisions created clear guidelines for employers selecting default investment options for workers who do not actively choose their retirement investments. These guidelines legitimized using more sophisticated default options beyond the traditional low-yield money market funds. Under the new framework, target-date funds, balanced funds, and professionally managed accounts could serve as default investments while protecting employers from liability.

This shift in default investment options aligned with the larger transition from actively managed defined-benefit pensions to more passively managed defined-contribution plans. While pension managers traditionally favored active management to boost returns and funding status, 401(k) participants typically gravitate toward lower-cost passive options. The QDIA framework supported this trend by enabling employers to automatically enroll workers into diversified, often passively managed investment strategies, fundamentally changing how Americans save for retirement.

By 2016, the changing retirement landscape prompted major updates to erisa’s fiduciary protections. At that time, with more than eighty million participants in defined-contribution plans, the Department of Labor significantly expanded the Fiduciary Rule and who counted as giving investment advice, requiring more financial professionals to act in their clients’ best interests. The rule covered onetime recommendations, rollover advice, and IRA guidance, creating new exemptions with strict conditions for advisers receiving commissions. Previously, a divide existed between being an adviser with fiduciary responsibility and a broker for whom the far more permissive “suitability” standard applied. Suitability merely required investment advice to be appropriate for the client but not necessarily in their best interest relative to all available options.

These shifts proved a boon for the largest asset managers, whose scale allowed them to create low-cost index products with rock-bottom fees. Consequently, a tremendous bifurcation arose within U.S. asset management. A handful of large firms won the bulk of new allocations, while smaller investment managers focused on active portfolio management experienced a secular decline. According to Broadridge Financial, a data firm focused on investment management, “Vanguard, Fidelity, and BlackRock manage just under 50% of total AUM, amounting to over $14.9 trillion. Over the past decade, these three firms have captured more than 50% of cumulative flows into their investment products. In 2023 alone, they received 71% of capital inflows in the US, compelling other fund complexes to adjust their pricing strategies accordingly.”10

The downward march of rates, combined with the demographic crest of baby boomers hitting their prime earnings years, has largely exhausted the growth of passive investing. Naturally, large asset managers have looked to less commoditized markets to continue growing their assets under management with higher-margin products. Greater distribution of private equity, forays into cryptocurrency, and, most successfully, expansion of private credit strategies have powered that growth. BlackRock now expects private credit assets under management to reach $3.5 trillion by 2028.11 Of course, this growth would not be possible without the realignment of lending markets following the 2008 financial crisis and the regulations it spawned.

Lending in the Sponsor Age

The 2008 global financial crisis fundamentally reshaped lending markets through both regulatory reform and market evolution. Basel III in Europe and Dodd–Frank legislation in the United States imposed more stringent capital requirements on banks, particularly for “riskier” loans. These regulations effectively sought to transfer risk from banks to market participants, with specific provisions targeting banks’ financing of private equity–sponsored businesses.

This regulatory shift accelerated an already emerging trend of bank disintermediation. The leveraged loan market provides a stark illustration—banks once held 70 percent market share in this category but today account for less than a quarter of leveraged lending. As banks retreated, particularly from middle-market lending, private credit managers stepped in to fill the void. This transformation shows no signs of reversing. New banking regulations on the horizon—Basel III Endgame in the United States and Basel IV in Europe—are expected to require banks to hold even more capital against their loan portfolios, possibly by as much as 19 percent in the United States and 24 percent in Europe.

Part of the challenge of identifying the influence and growth of private credit is that it elides concise definition. Private credit simultaneously rejects and appeals to these vague definitions depending on the context. John Zito of Apollo Global Management, speaking at the Grant’s Private Credit Conference in March of 2024, used french fries and Wikipedia to illustrate the point. French fries, Zito explained, take a variety of forms and can be prepared in a multitude of ways. He noted that the Wikipedia page for french fries has a word count of nearly four thousand and has been edited over 1,400 times. Private credit, undoubtedly more complex and varied, has just five hundred words and less than one hundred edits. Zito’s point: “We need to make private credit more like french fries,” meaning that the investment community should appreciate and segment the multiple expressions of private credit, which is, after all, just lending. At the same time, private credit promoters like to use the broadest possible definition when discussing asset growth or credit metrics. For example, Zito said that less than 15 percent of private credit was below investment grade, no doubt relying on a more inclusive definition of the asset class.

The middle market, comprising roughly 200,000 companies with revenues between $10 million and $1.1 billion, represents one-third of the U.S. private sector GDP and employs forty-eight million workers. As banks scaled back their presence in this segment, private credit funds emerged as vital providers of capital, offering more flexible terms and tailored financing solutions compared to traditional bank lending.

The concurrent growth of private equity created natural demand for these new lending sources. Private equity sponsors sought additional capital to finance their expanding activities, particularly in an environment where timely and flexible financing became increasingly valuable. Private credit managers capitalized on this opportunity, establishing themselves as key players in financing leveraged buyouts and other private equity–driven transactions.

Private credit has competed with banks in terms of speed, certainty, and discretion, but not necessarily price. For large loans, generally defined as those greater than $2 billion, banks have historically relied on the broadly syndicated loan market (BSL). For large loans, the choice of syndicated loan versus private credit is fluid and more competitive than direct relationship lending with banks. As loan sizes come down, the two capital sources become more distinct. Syndicated loans have tighter spreads and slightly more borrower-friendly terms. Conversely, private credit, in the form of bilaterally negotiated transactions, has greater lending protections and higher spreads. Under those conditions, it may seem odd that private credit has been a more popular avenue than syndicated loans, but private credit’s bespoke offerings are worth the price to certain borrowers. Namely, private equity sponsors are looking to push the limits of leverage ratios and value the ability to negotiate loan terms on a one-to-one basis.

In recent years, a more tepid deal environment for private equity and a general reluctance to bring companies to the public market has shifted the application of credit from financing transactions to financing liquidity. With equity markets at all-time highs, one might ask why private equity firms are not eagerly taking their portfolio companies public. According to Apollo’s Zito, at issue is the largest multi-strategy hedge funds, which control nearly $1 trillion of equity flows when accounting for leverage. Those firms are not interested in buying newly issued shares of companies in which a private equity sponsor will own a large percentage of the float. The tight risk management controls of these firms mean they cannot risk a dearth of buyers should they need to exit their positions.

With nearly $2 trillion deployed, private equity funds must generate distributions for their LPs. According to Zito’s estimate, they should be looking to return $1 trillion over the next year and are $850 billion short of that goal. Funding distributions through a form of private credit-financed dividend recapitalizations is an increasingly attractive option.

As a result, private equity firms have gotten more creative in what they will lend against and how they structure such loans. That has meant an intentional foray into asset-backed lending. Banks and other institutional investors have historically financed debt related to education, car loans, equipment, and credit cards. Private capital is looking at assets like music royalties, movie rights, and hard assets like airplanes and GPU clusters. According to an April Bloomberg report, asset-backed deals collateralized by “unusual collateral” have risen considerably in the post-pandemic era.

Esoteric ABS deals—backed by collateral other than student, auto, credit card and equipment loans—have risen to about 31% of the ABS market from 9% over the last decade, according to Barclays Plc. Collateral pools have also become more diversified, with investors seeking out novel structures to earn excess returns as ABS spreads tighten, dropping more than 30 basis points since November. Meanwhile, interest rates are expected to stay higher for longer, meaning the benefits to borrowers of waiting to come to market have dissipated.12

In May, Blackstone, alongside several other private funds, originated a $12 billion loan to CoreWeave. CoreWeave launched in 2017 and began amassing Nvidia Graphical Processing Units (GPUs) ahead of the boom in artificial intelligence (AI) investments. While CoreWeave’s original business plan focused on mining cryptocurrency, they shifted their model in 2020 to focus on the burgeoning AI space. The company claims to be the largest private operator of Nvidia GPU clusters in the United States, with over forty-five thousand chips.13 The new capital will go toward buying thousands more.

Unlike a traditional loan in which the debt is serviced from company cash flows, the Blackstone loan moves the chips into a “metaphorical lockbox, housing all of CoreWeave’s AI chips. Any revenue the company generates from clients using those chips, the most advanced of which cost tens of thousands of dollars each, goes first toward paying its lenders. Any excess cash after making the loan payment flows to the company as net revenue.”14 The loan itself is collateralized by the chips and not all company assets.

Mike Nowakowski, head of structured products at Conning, told Bloomberg that the relative lack of historical data usually demands concessions to the benefit of investors. He added that insurance companies have started looking more closely at these deals as they get more creative with deploying capital.

This focus on collateral lending, as opposed to productivity or repayment ability, is another sign of runaway demand for debt securities. It conflates funding with wealth creation; the goal of debt becomes a form of asset capture versus productivity or growth.15 This is driven by a demand for return without accompanying risk, exactly the kind of investment that prospective retirees seek when they enter an annuity contract.

Marriage of Private Credit and Insurance

In recent decades, as pension assets declined, alternative asset managers began looking for ways to access the growing market of defined-contribution retirement plans. Success in accessing traditional 401(k)s and IRAs has been limited, however, as the Obama Department of Labor expanded the fiduciary rule to include these vehicles, where previously they were excluded. Concerns about higher fees and conflicts of interest discouraged plan sponsors from recommending active or complicated strategies and potentially opening themselves to liability and litigation. An Information Letter in June of 2020 from the first Trump administration’s Department of Labor stated that the department “believes that a plan fiduciary of an individual account plan may offer an asset allocation fund with a private equity component.”17 A supplementary letter in December of 2021, under the Biden administration, hedged those comments as the industry viewed them as a wholehearted endorsement of private equity in retirement savings plans. The supplementary letter reinforced the fiduciary obligation of plan sponsors, “cautioning fiduciaries—especially in small plans—against marketing efforts that may misrepresent the Information Letter as a U.S. Department of Labor endorsement or recommendation of these investments for 401(k) plans.”18

Caught between competing visions of fiduciary duty, alternative asset managers turned their attention to the insurance market. Under the large tent of insurance, a spectrum of liabilities ranges from simple to actuarially complex. Complex liabilities include products like long-term care insurance and property and casualty lines. Simple liabilities are more akin to investment products like annuities and pension liabilities. While insurance is capital intensive and highly regulated at the state level, its products remain outside the reach of the fiduciary rule. Moreover, the structure of long-term insurance liabilities creates a form of fixed-rate financing for investment activities.

Private equity’s foray into the insurance business began after the 2008 financial crisis. Lower rates intended to spur an economic recovery caught insurers off guard, and they struggled to generate returns as spreads between the rates at which policies were issued and the rates offered by investment-grade securities compressed or even inverted. Private equity offered insurance companies capital infusions and access to riskier, high-yielding investments. Buying insurance liabilities offered alternative asset managers a perpetual pool of capital to feed into their investment products and a large asset base subject to fees. Initially, private equity firms took large stakes in insurers to influence their asset allocation, but increasingly, they wholly own insurance or reinsurance franchises. According to A.M. Best, by the second half of 2023, private equity firms owned $774 billion in life insurance assets—or 9 percent of life insurance industry assets.19

No firm has pursued insurance assets as aggressively as Apollo Global Management. Since its 2009 purchase of American Equity Investment Life, Apollo has grown its Athene & Athora insurance franchises to $374 billion, over 50 percent of its $733 billion in total assets. “Spread-related earnings,” Apollo’s term for its earnings on insurance assets, now represent 60 percent of its combined fee and spread-related earnings.20 Apollo fully merged with Athene in 2021, becoming the first major alternative asset manager to bring insurance fully onto its balance sheet. Despite initial skepticism, Apollo’s market capitalization has tripled since the transaction. Understanding Apollo’s success requires reckoning with the complexity they have brought to the insurance value chain.

Nearly every major alternative asset manager found a way to enter the insurance market following the 2008 crisis. Yet the economics of managing insurance assets are considerably less attractive than those of alternative managers’ core business. While a private equity fund may have fees between 1 and 2 percent of assets and receive carried interest over a hurdle rate, the capital requirements of insurance mean that only a small portion of the total can go into alternative managers’ flagship funds.

Insurers are regulated at the state level, but the National Association of Insurance Commissioners (NAIC) has a set of standardized guidelines that dictate capital requirements for different types of insurance. The risk-based capital requirements for insurers are complex and granular, splitting assets into twenty different risk buckets. Broadly speaking, for annuity assets, 85–90 percent of the capital must be in investment-grade fixed-income securities, with 10–15 percent available as equity capital to the insurer. The alternative investment manager can only charge de minimis fees (40 basis points or less) on the private investment grade portion of insurance capital. The equity, however, can be invested in their higher margin offerings. For alternative managers, making insurance assets a high-quality revenue stream like their core asset management business requires massive scale. That scale requires a high volume of private debt origination, either sourced or developed organically.

In this interplay between the equity capital that insurance assets create at the bottom of the capital stack and the need for private investment-grade debt origination at the top, Apollo was able to innovate around the traditional private equity model. Apollo CEO Marc Rowan saw something vital in the sleepy old model of insurance. Rowan told investors at the Barclay’s Global Financial Services conference in September,

That is the single biggest constraint on growth, not capital formation, not how many people you have. It really is built around can you originate enough attractive assets to you to meet your needs. And that’s why we have been so focused and in fact, some might say maniacally focused on really making sure we are building the right type of origination in the right volumes, looking for the right new places to be doing that because our whole business is about delivering excess return per unit of risk.

To address the origination constraint, Apollo has used the equity that “falls out” of the insurance structure, then raises outside capital in the traditional private equity model to capitalize, purchase, or otherwise finance captive debt origination platforms. Apollo, in effect, leverages their insurance equity via the private equity structure to earn fees and carried interest on the debt those platforms are originating. The portion of that debt origination that qualifies as investment grade can be fed back into the top of the insurance capital stack, dropping down new equity that is used to equitize further debt origination.

This makes the normally capital-intensive nature of debt origination considerably more efficient. Whereas in the traditional model, a dollar of insurance assets may only generate ten cents of equity to invest, Apollo’s model can turn those ten cents of equity into thirty or forty cents of equity by running it through a private equity structure. It introduces “Other People’s Money” (OPM) at every step of the insurance capital value chain. As a hypothetical example, an insurer can pair $5 of insurance equity with $5 of sidecar investment, then use their $5 of insurance equity to create an evergreen fund split 70/30 with outside investors, creating $7 of new equity. That new equity can go into a 50 percent joint venture debt origination platform, turning $5 dollars of insurance equity into $14 of equity that supports the origination of new credit to feed back into the structure.21 This equity is earning fees and carry closer to traditional private equity, but crucially, it is doing so with long-term, fixed-rate capital generated from the growing annuity market. This is an admittedly simplified illustration of the complexity of Apollo’s model, yet it can be reduced to a cascade of leverage, starting with the insurance liability and moving through to the private equity structure, which is itself a form of implicit leverage.

Apollo and its assets are still small in the grand scheme of financial markets and even within retirement assets. Nevertheless, it has, in no small measure, sparked an arms race among traditional asset managers to build in-house private credit origination capabilities. In December, BlackRock agreed to buy HPS, a private credit manager with $128 billion in assets, for $12 billion dollars. Apollo itself increasingly looks up-market with its lending activities.22 Its ambitions transcend middle-market lending to directly serving highly rated multinationals like AT&T, Intel, and AB InBev. Again, instead of funding these companies at the corporate level, Apollo focuses on “unique projects or strategic objectives better served by customised structured financing. Each deal has different terms but all transform a cash flow waterfall into investment-grade debt that is supposed to simultaneously solve a challenge for the Apollo counterparty, support retirement savings of Athene’s elderly customers and give Apollo a higher rate of return for its shareholders.”23

Unlike banking, which has an inherent duration mismatch between short-term depositors and long-term borrowers, Rowan argues that Apollo’s form of lending is less risky because duration can be more or less matched to each pool of capital that Apollo serves.24 While that may be true, private credit has not supplanted bank lending as much as it has exploited it. Banks often find themselves providing warehouse lines or other forms of credit to the very funds that they compete against for lending.25 Citi has even partnered with Apollo to leverage its investment banking workforce to source loans that will be funded with Apollo’s capital.26 So-called alternative investment managers like Apollo now find themselves with greater power than the nation’s money center banks. They have artfully cut a path that avoids the most onerous regulations of banking, blurs fiduciary lines, yet still benefits from the implicit guarantees typically reserved for highly regulated institutions.

The End of Savings

Just as pensions gave way to defined-contribution retirement plans, the tripartite trends of private credit, insurance, and demographics set the stage for annuities to replace traditional savings invested in equities and liquid fixed income. That has important implications for growth and economic dynamism. Capital markets risk becoming subsumed by the demand for debt securities. In theory, capital allocation moves capital from bad allocators to good and ultimately from low-return projects to higher-return ones. That process has historically been driven by a willingness of the market to take equity risk, and the appetite for such risk seems to be in long-term decline.

“Replacement” is a term repeatedly invoked by Apollo in conference calls, interviews, and promotional videos. Replacing public equity with private, replacing corporate debt with private credit, replacing equity with fixed income, and ultimately replacing savings with insurance. Equity in the insurance model is more akin to a derivative or an option that derives its value from asset prices and credit spreads. Alternative managers run this equity through a private equity structure that further detaches investment outcomes from business performance.

Under this model, equity exists to serve the creation of debt. Resource and capital allocation are not front and center. This form of finance values greater origination volumes both to support asset prices and to feed new assets into the top of the insurance balance sheet. This system undermines the simplistic belief that the capitalist system works via the capital allocation feedback mechanism. Instead, the self-perpetuating demand for debt instruments continually supports asset prices.

All forms of debt borrow from future growth. When that growth fails to materialize, new debt is needed. As diminished expectations weigh on returns, yields need to be structured to continue to attract capital. Structured finance takes a given yield and then tranches it into a priority of payments, creating higher and lower yielding securities by breaking risk and reward up into new buckets. The riskiest of those buckets is the equity tranche, which bears the first loss in the event of a payment shortfall. Insurance-led credit origination takes a debt, the annuity liability, and uses a portion of it to serve as the equity of new debt vehicles.

Without credit contraction, asset price reckoning is forestalled. This reduces the theaters of speculation to corners of the market without debt‑driven asset prices—cryptocurrency, venture capital, and a smaller cohort of traditional equities. Savers are increasingly attracted to instruments that offer defined outcomes that truncate the distribution of returns (insurance products in a different wrapper). The demand for increasingly esoteric forms of collateral supports a growing market for consumer finance products that can be securitized. A dystopian view might be a world where there are no savings-funded investments; rather, savers purchase insurance products like annuities. Those insurance products are fed by the debt created from savers’ levered consumption. While not inherently calamitous, this transformation carries risks for economic vitality. By favoring debt, collateral-based lending, and guaranteed returns, the system may direct less capital to productive equity investments. In this debt-centric paradigm, real economic growth plays a shrinking role in justifying ever-larger pools of investment capital. The upshot is a finance industry that thrives, not on discovering new opportunities for value creation, but on feeding its own self-perpetuating demand for yield—a modern-day ouroboros that may gradually erode the dynamism of the real economy.

This article originally appeared in American Affairs Volume IX, Number 1 (Spring 2025): 3–17.

Notes

1 Daniel Peris, “The Retreat of Dividends and the Changing Nature of the Stock Market,”

American Affairs 6, no. 3 (Fall 2022): 3–22.

2 Mike Green, comments at the 2024 Grant’s Investing Conference, New York, October 1, 2024.

3 Torsten Slok et al., The Growing Retirement Savings Challenge (New York: Apollo Global Management, November 2024).

4 “Limra: Record-High 2023 Annuity Sales Driven by Extraordinary Growth in Independent Distribution,” limra, March 12, 2024; limra, Preliminary U.S. Annuity Third Quarter 2024 Sales Estimates (Windsor, Conn.: limra, 2024).

5 Dan M. McGill, Guaranty Fund for Private Pension Obligations (Homewood, Ill.: Richard D. Irwin, November 1970).

6 Jennifer K. Elsea, The Insurrection Act and Related Authorities: A Brief Overview, CRS Report No. IF12007 (Congressional Research Service, December 15, 2022).

7 William A. Birdthistle, Empire of the Fund: The Way We Save Now (Oxford: Oxford University Press, 2016).

8 Donovan v. Bierwirth, 680 F.2d 263 (2d Cir. 1982).

9 Felix von Moltke and Torsten Slok, Assessing the Impact of Passive Investing over Time: Higher Volatility, Reduced Liquidity, and Increased Concentration (New York: Apollo Global Management, November 2024).

10 Broadridge, US & European Fund Fee Trends; Exploring a Decade of Transformation (Lake Success, N.Y.: Broadridge Financial Solutions, 2024).

11 BlackRock, Private Debt: The Multi-Faceted Growth Drivers (New York: BlackRock, September 2024).

12 Immanual John Milton and Carmen Arroyo, “Credit Investors Snap Up Bonds Backed by Art Loans, Internet Addresses,” Bloomberg, April 4, 2024.

13 Tabby Kinder, “Wall Street Frenzy Creates $11bn Debt Market for AI Groups Buying Nvidia Chips,” Financial Times, November 4, 2024.

14 Asa Fitch and Miriam Gottfried, “How Wall Street Lenders Are Betting Big on the AI Boom,” Wall Street Journal, May 21, 2024.

15 Savvakis C. Savvides, “The Disconnect of Funding from Wealth Creation,” World Economics Journal 23, no. 2 (June 2022).

16 Eileen Applebaum, “As Public Pensions Shift from Hedge Funds, Hedge Funds Look to Main Street,” Hill, November 30, 2015.

17 Stephen Miller, “DOL Pulls Back on Private Equity in 401(k)s,” SHRM, January 11, 2022.

18 Miller, “DOL Pulls Back on Private Equity in 401(k)s.”

19 Andrew Park and Patrick Woodall, Risky Business: Private Equity’s Life Insurance Gambit (Washington: Americans for Financial Reform Education Fund, December 2023).

20 Apollo Global Management, Apollo Global Management Inc. Reports Third Quarter 2024 Results (New York: Apollo Global Management, November 2024).

21 “Trading Complexity for Capital Intensity in Life Insurance,” Red Deer Investments, July 7, 2024.

22 Eric Platt and Antoine Gara, “BlackRock Agrees to Buy Investment Firm HPS in $12bn Deal,” Financial Times, December 3, 2024.

23 Sujeet Indap and Eric Platt, “Apollo Pushes into High-Grade Debt Business Long Dominated by Banks,” Financial Times, September 16, 2024.

24 William Cohan, “Apollo’s Mission in Finance,” Financial Times, June 17, 2023.

25 George Steer, “Banks and Private Credit: Best of Frenemies?,” Financial Times, November 22, 2024.

26 Eric Platt and Stephen Gandel, “Citigroup Strikes $25bn Deal with Apollo to Launch Private Credit Venture,” Financial Times, September 26, 2024.