Artillery shells are not particularly complicated munitions: an HF-1 steel casing containing IMX-104 or TNT explosive, a fuse, and a propellant charge. But after more than two years of attempting to scale up production to supply Ukraine’s defensive line, the world’s largest economy has come nowhere close to meeting the monthly requirement: 360,000 rounds.1 At the start of the war in February 2022, the United States could produce 14,400 per month; by December 2022, 28,000; by March 2024, 30,000.2 The Biden administration is desperately trying to spin as an achievement the fact that the U.S. defense industrial base (DIB) is currently on track to produce 100,000 rounds monthly by summer 2025: more than three years into the war, and not even a third of the way to the target.3

According to the Army War College, the U.S. entered the Korean War in 1950 with a stockpile of six million 155 millimeter shells; even as late as 1980, the defense industrial base could churn out 84,000 shells per month—with wartime surge capacity of over 430,000.4

The 155 millimeter shell has become the most visible symbol for contrasting these two eras. Ironically, focusing American anxiety just on “missile gaps” is a luxury we can no longer afford, nor even on the “shipyard gap” with China; we now have to worry about basic ammunition deficits.

During the unipolar moment, DIB policy attracted interest only from niche circles within the military and foreign policy elite. Following the USSR’s 1991 collapse, the Pentagon could readily deal with emergent military threats both at a fraction of the relative cost (as a percentage of GDP) and force level of the Cold War period. Of course, history caught up in ways now well understood. The phrase “great power competition” has lately become so tiresome to print that it’s frequently abbreviated “GPC.” China’s economic rise enabled an unprecedented military buildup, both nuclear and conventional, by the People’s Liberation Army. Russian forces invaded Crimea in 2014, followed by the latest, ongoing offensive that began in 2022. Conflict resurfaced in the Middle East in 2023—with Iranian proxies sowing terror in Israel and harassing global shipping lanes.

It has become clear that the current DIB is ill-equipped to produce materiel adequate to achieve plausible mission objectives in any one theater America is currently engaged in, let alone all three. Even those counseling retreat into a reprised Monroe Doctrine will find current production inadequate for credible homeland defense. Paradoxically, however, despite DIB reform receiving more attention in Washington—it is perhaps the sole issue enjoying rare bipartisan congressional, presidential, and media focus—significant legislation and decisive policy change remains elusive.

The Munitions Gap as a Coalitional Problem

For some, the lack of action is a question of policy priorities: a failure to adequately prioritize defense spending as a share of the discretionary budget. For others, it’s an institutional question, concerning the Pentagon’s risk-averse culture and bureaucratic inertia. Still others suggest that it’s ultimately an ideological question: Americans have lost the moral and patriotic fiber to support the country’s postwar stewardship of the “international order.” Few, however, understand this otherwise puzzling inaction as primarily a coalitional problem: in other words, there is simply not a powerful enough corporate-political base, broadly distributed across a critical mass of states, with an interest in modifying the current system.

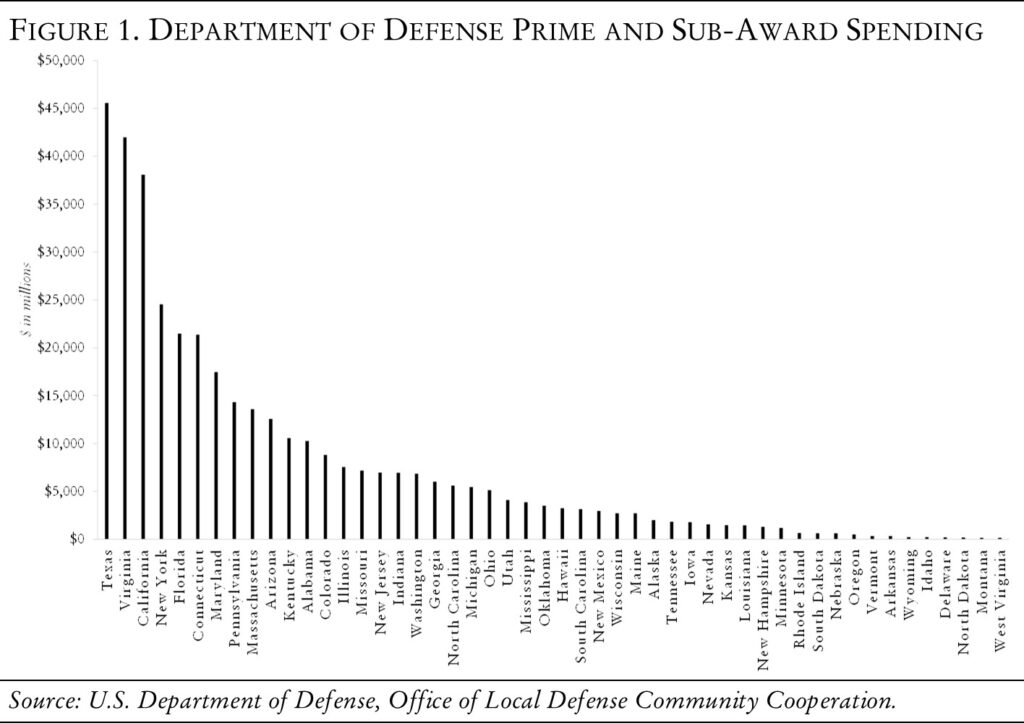

An underdiscussed fact: as of fiscal year 2022, the latest for which there is available data, Texas, Virginia, and California alone received nearly a third of defense prime and sub-award contract dollars. The top ten states received nearly 60 percent, and the top ten counties receive roughly 15 percent, more than the bottom twenty-five states, which receive only 10 percent. Put in political terms: when a full half of the U.S. Senate has less material incentive to tackle reform than a handful of colleagues in the House of Representatives, it’s little wonder why Congress hasn’t rushed the issue to the top of its priority list.5

This coalitional perspective offers a distinctive lens through which to view both the history of the U.S. defense industrial base as well as forward-looking prescriptions for reform. In brief, the history of twentieth-century American defense readiness and reform is, in large part, a history of relocating investment from the Rust Belt to the “Gunbelt” (the Sunbelt, flanked by the coasts). Concentrated industrial geographies, through political compromises, gave way to a greater dispersal toward the industrial frontier. But policymakers today have largely ignored this historical pattern, underrating the need for (and therefore neglecting to identify) new geographic coalitions favoring reform (which, in turn, translate into lobbies for durable congressional majorities). A better approach would take this lesson into account.

Rise of the Gunbelt: 1938–93

Popular historical memory tends to associate mobilization for World War II with the midwestern industrial core; the war, in this narrative, was ultimately won in Detroit. This is partly true, but few remember the New Deal political compromise with the typically isolationist South that enabled early mobilization in the first place.

As Arthur Herman points out in Freedom’s Forge, the American defense industry in the 1920s did not at all reflect the country’s underlying industrial strength. Following World War I, the Nye Commission’s highly publicized investigation into American defense contractors concluded with a call for nationalizing the defense industry. This didn’t occur, but support for defense production was at such a low ebb by the onset of the Great Depression that there was no objection to Herbert Hoover’s deep cuts to military spending.6 The New Deal coalition that came to power in 1932 had no interest in changing that trajectory. Southern Democrats, key to President Franklin D. Roosevelt’s electoral coalition, led the passage of the Neutrality Acts of 1935 and 1936, which banned the sale of any American materiel to nations at war.

Sentiment began to change, however, as the first New Deal sputtered and Germany threatened Great Britain’s shores. Nazi control over the Royal Navy might threaten American shipping, just as unrestricted submarine warfare had in World War I. But the U.S. political system remained gridlocked between a “nationalist” faction primarily focused on manufacturing for the domestic market, behind high tariff walls, which remained skeptical of intervention, and an “internationalist” faction, led by the ascendent auto sector, which had mastered continuous flow production and sought greater market share abroad. FDR, increasingly convinced that America might eventually have to intervene, supported rearming but was politically hamstrung.7

Alongside Senate Majority Leader Alben Barkley (Kentucky), Speaker of the House Sam Rayburn (Texas), and rising star Representative Lyndon B. Johnson (Texas), FDR’s solution was to lay a foundation for a new political coalition by expanding the American manufacturing core toward the South and West, what is typically known as the “Sunbelt.” As Johnson put it, “Texas not only wants to do everything it can for defense, but it foresees the need for preserving and expanding its manufacturing plants for normal demands of the future.”8 Previously unpopular projects, such as the Tennessee Valley Authority, found new justification in the name of national security. The War Production Board and National War Labor Boards also pushed policies that decentralized factory supply chains throughout the continental United States, raising wages for western and southern labor. As Harvey Perloff estimated, at the start of the twentieth century, 74 percent of U.S. manufacturing employment was located in a “manufacturing belt” in the Northeast and eastern Midwest; after this political compromise, this region still retained 64 percent (of a larger overall manufacturing workforce), but the concession to share the growth was significant enough for Southern Democrats to back FDR’s mobilization.9

As the military transitioned from World War II to the Cold War, the ability to conduct industrial warfare (both on the ground and via “strategic bombing”) remained important, but in the new atomic era it increasingly competed with an emphasis on missile and space forces. During the trade surpluses of the 1950s and ’60s, as well as the boom years of the 1980s, both could be accomplished with minimal tradeoffs. For example, the Scranton Army Ammunition Plant, which until recently was the sole producer of 155 millimeter shell casings for the entire U.S. military, was originally a railroad repair shop purchased in 1951 by the U.S. Army to produce ordnance for the Korean War.10 During the same era, in 1950, Colorado Springs won the bid to host Air Defense Command, precursor to North American Aerospace Defense Command and U.S. Space Command, and in 1954 won the bid for the U.S. Air Force Academy.11

The late Cold War’s move even further away from industrial warfare, toward moonshots like Reagan’s SDI, solidified the move toward the Gunbelt and away from the Rust Belt and even much of the New Deal South. At this point, the geographic orientation of U.S. defense favored higher-tech California, Colorado, Texas, Alabama, Virginia, and the R&D powerhouses of the Northeast. And with the end of the Cold War, the funding tide would go out, forcing a period of painful industry—and geographic—consolidation.

Tightening the Gunbelt: 1993-2011

Domestic political pressure for a “peace dividend” after 1991 resulted in reductions in the defense budget. At the famous 1993 “Last Supper,” William Perry, then deputy secretary of defense, pressed for significant consolidation in the Pentagon’s network of prime defense contractors.12 The industry swiftly followed that trajectory—shifting from over fifty primes in the early 1990s down to roughly five at present.13 Geographically, the defense industry as a whole took a revenue hit, further driving the mergers and acquisitions frenzy. Congressman Dick Armey led the movement for establishing the Base Realignment and Closure Commission (BRAC) in 1988, leading to five rounds of base closures, a total of 350 facilities. Consolidation made offshoring capital-heavy supply chains more attractive. The dynamics set in motion at this time largely explain why the United States currently does not produce any M6 propellant or maintain any domestic TNT plants to make explosive filler for 155 millimeter shells.14

But for three decades, these developments could be ignored. What little discernible impact offshoring trends had on U.S. military readiness could be remedied through ad-hoc infusions of defense spending and were further obscured by the absence of any great power threats. Defense spending increases after 9/11, which, combined with the relatively small scale and sequencing of the wars in Iraq and Afghanistan, did not place acute strain on the DIB.15 Even mistaken obsessions with “wonder weapons” to fight counterinsurgency campaigns could go unnoticed. Donald Rumsfeld, for example, canceled “dumb” self-propelled howitzers, which fired traditional 155 millimeter rounds, in favor of “smart” Excalibur rocket-assisted guided munitions, which cost $100,000 each—though their GPS, as the Ukrainian army has learned, can be easily jammed by enemies.

Further minimizing the impact of any supply-chain disruptions, defense planners could rely on strategies of “iron mountains” designed to overwhelm opponents with massive, gradual force capability buildups—such as the “AirLand Battle” doctrine in the First Gulf War and its “Full‑Spectrum Operations” descendant—that accommodated longer lead times for suppliers.16

At the turn of the decade, however, these conditions inverted: the defense budget flatlined and great power threats reemerged. Anxiety about the U.S. fiscal deficit following the 2008 Great Recession resulted in the 2011 Budget Control Act (BCA) and its successor, the 2023 Fiscal Responsibility Act (FRA), which placed procedural controls around increasing defense spending—resulting in a flat (even declining, in real terms) Department of Defense (DoD) budget. Having shed its capacity for conventional industrial production over three decades, a tightened, sclerotic Gunbelt had no answers for the return of land war in Europe, another outbreak of hostilities in the Middle East, and China’s manufacturing dominance.

Four Dead Ends

There’s no shortage of think tank proposals to address DIB and supply-chain deficiencies. Despite favorable bipartisan sentiment, however, many are unlikely to muster sufficient corporate lobby or congressional support, which are highly correlated. In simplified terms, these recommendations might be grouped within four broad verticals: (1) greater spending, (2) technocratic adjustments, (3) executive action, and (4) antitrust policy.

Most simplistically, many analysts call for significantly greater spending, or freeing the defense budget from the constraints of the Fiscal Responsibility Act in order to increase the top-line budget under the existing procurement regime. These voices also frequently highlight the need to provide the defense budget “on time” by avoiding budgets passed by continuing resolutions, which lead to both unstable and uncertain demand signals for suppliers. Attempts to compensate for DIB deficiencies with sustained levels of increased top-line spending, however, face considerable political obstacles, especially given the 2023 Fiscal Responsibility Act’s restoration of budget caps for fiscal year 2024–25.17

To take a recent example, Senator Roger Wicker’s much-discussed proposal (a significant upfront top-line increase in fiscal year 2025, followed by sustained marginal increases over the next five to seven years until levels reach 5 percent of GDP) cannot narrowly address DIB underinvestment without triggering a broader fight over the federal budget as a whole. Even the modest $25 billion increase that Wicker was able to push through 2024’s Senate Armed Services Committee NDAA markup was immediately opposed by Democrats.18 In response, Wicker presented this as a “starting point” for negotiations, but it seems highly unlikely that any compromise will involve an upward revision toward Wicker’s preferred $55–$950 billion increase.19

Others focus on advancing technocratic adjustments to the Pentagon’s procurement system. This group’s favored proposals center on both incentivizing greater capital expenditure from suppliers and greater competition for contract awards. For the former, this group counsels an increase in multiyear procurement contracts and “block buys,” while simultaneously reducing “indefinite delivery, indefinite quantity” (IDIQ) contracts, allowing for greater procurement predictability. For the latter, this group focuses on eliminating bureaucratic red tape, burdensome regulations, and expanding the use of Other Transaction Agreements (OTAs) to enable “greater innovation” and greater procurement speed, as well as opening the procurement process to more players. The most powerful corporate or political lobby interests for these agenda items, however, are vested in the status quo, and maintain political leverage over the budget and procurement process. The business models for most plausible insurgent sponsors—primarily smaller defense contractors—rely substantially on subcontracting for primes.

Other reformers focus on executive action, prioritizing policy options at the president’s direct disposal—especially via the Defense Production Act (DPA) and Section 301 trade authorities—paired with agency-level reforms and adjustments to international bodies. These types of tools might include, inter alia, expanding cooperation and harmonizing regulations with members of the National Technology Industrial Base (NTIB), Five Eyes, Quadrilateral Security Dialogue (QSD), Indo-Pacific Economic Framework (IPEF), and/or AUKUS to expand co-productive capacity. Others call for creating a dedicated undersecretary and/or dedicated offices within the Department of Commerce to routinize and harmonize usage of DPA Title III, which “authorizes appropriate incentives to create, expand or preserve domestic industrial manufacturing capabilities for industrial resources, technologies, and materials needed to meet national security requirements.”20

Policy levers at the White House’s unilateral disposal, however, are best seen as amplifiers of already appropriated funds—not substitutes for them. For example, even as the Biden Administration has used DPA tools to secure commitments from manufacturers to surge munitions production capacity, they cannot deliver on them without new funding on the other end.21 This is in part the result of the relative scarcity of government-owned, government-operated (GOGO) and government-owned, contractor-operated (GOCO) facilities. Additionally, the practical state capacity and manpower needed to actually implement reforms at the necessary scale requires financing support from Congress and, ideally, from the states; DPA tools alone will likely have only marginal effects. Finally, while attempts to leverage the collective power of international bodies—such as NTIB, AUKUS or IPEF—to address market destabilization might eventually be necessary, the combination of their highly technical nature and detachment from Congress make them suboptimal catalysts for reform.22

Still others call for more aggressive antitrust action. DoD undertook an internal review on the “State of Competition within the Industrial Base” in February 2022, which might serve as a premise for these efforts.23 These types of tools include more aggressive Federal Trade Commission (FTC) actions to break up major defense primes, or at least limit further consolidation within the industry; ceasing “contract-to-monopoly” practices that award large munitions contracts to single manufacturers and, conversely, expanding the use of models based on the U.S. Army’s Medium Caliber Family Acquisition (MCFA), which spread awards to multiple facilities; and procuring the intellectual property for major end products (platforms, munitions, etc.) and then contracting to multiple manufacturers and integrators for production.

Yet, as with antitrust policy in general, incumbents within a sector—in this case, defense primes—have massive legal resource advantages over the FTC, Department of Justice, etc., significantly degrading timely action and diminishing its effect. Further, even if these efforts had positive effects in the longer term, they might hamstring efforts to efficiently scale up production in the near term. Given the urgency required to rapidly address even minimal conventional threats, this approach could be imprudent. Further, as discussed above, given that potential corporate candidates for a “counter-prime” political coalition are often subcontractors for primes (and therefore dependent upon them), congressional means for advancing this agenda are limited.

Solution: A Greater Gunbelt

The baseline deficiency of these four approaches to reform is that they are not primarily optimized to generate a new geographic coalition. Given the historical pattern of creating a new defense coalition by building partnerships with the industrial frontier, it would seem that the next natural strategy would be to focus on rebuilding the DIB in the deindustrialized Rust Belt. Nevertheless, this strategy likely will not work. The Gunbelt’s initial rise occurred when the United States was capable of being a surplus manufacturing economy, and its Cold War surge coincided with a deregulatory regime, both of which allowed the fiscal room for using public funds to create entire industrial ecosystems in new regions. Neither of those conditions exist today, and these limits have been codified in the aforementioned BCA and FRA.

Given these interlocking fiscal and legal constraints, the best political approach would not be to create a “new Gunbelt,” but to expand the web of suppliers, both numerically and geographically, that stand to benefit from reversing DIB underinvestment: a “greater Gunbelt.” The most effective way to generate such a coalition is not by focusing primarily, as most proposals do, on increasing appropriations and generating efficiencies affecting the procurement of full weapon systems (or even relatively high-value-added commodities such as semiconductors) but rather on the defense industrial “sub-base” (DISB), or the domestic market for lower-value-added inputs to those higher-value projects—such as minerals, alloys, plastics, oil, electrical components, active pharmaceutical ingredients (APIs), and so forth.

In sharp contrast to relatively narrow legislative efforts such as chips, reforms targeting the DISB have much more expansive appeal to both political and private sector actors. Consequently, broadening the coalition—the political base—for DIB reform by focusing policy intervention a level down—at the DISB—increases the probability of political success for timely and durable reform. While private sector lobbies for higher value-added inputs tend to be highly concentrated both in terms of market share and geographic distribution (limiting their utility in attracting congressional support), it is by comparison much easier to generate, for instance, a raw materials lobby spanning necessary majorities, if not supermajorities, of states and their legislators by focusing on the DISB.

This is because DISB reform generates specific, manageable development goals that are attractive to a much wider array of adjacent players, investors, and their political representatives. Approaches that promote solutions to the procurement or permitting systems at a more abstract level can be useful, but a project-based approach makes lobby interests more legible, and therefore easier to link with plausible coalition allies. For example, on September 12, 2023, the Department of Defense awarded a $90 million grant via the Inflation Reduction Act to Albemarle Corporation to expand lithium production in Kings Mountain, North Carolina, which had closed in the early 1990s.24 Two weeks later, on September 27, Albemarle and Caterpillar announced an agreement to collaborate on battery-powered mining equipment, using Kings Mountain lithium in future Caterpillar batteries.25 In May 2024, Albemarle and Martin Marietta Materials announced an agreement through which by-product limestone extracted from Kings Mountain would be repurposed for use in Martin Marietta’s construction aggregate (usable across a wide range of infrastructure and residential projects).26 Further, Albemarle announced an initial $1 million dollar donation to Cleveland Community College to support training and workforce development for Kings Mountain.27 Together, these three companies are directly linked to three congressional districts (Raleigh, North Carolina; Charlotte, North Carolina; and Irving, Texas) and four senators, and are connected to dozens of other representatives via their additional business and employees across other states. This allows these players to convert government relations resources into a ready-made lobby to push for the thirty estimated federal, state, and municipal permits required to begin production, as well as further tax breaks, subsidies, and workforce training.28 It is difficult to imagine generating this lobby without a specific project around which interests could converge: successful DISB reform would leverage this kind of model.

The core goal of DISB reform would be threefold. First, it would lower DIB input prices by pulling demand forward and stabilizing supply. Second, these lower prices would trigger mandatory, parallel adjustments to the Congressional Budget Office and DoD’s budgeting statistics, increasing in real terms the purchasing power of the current defense budget. Third, and relatedly, the funds “freed up” by these revisions would provide Congress and Pentagon war planners greater immediate leverage to be more ambitious and aggressive in issuing new contracts, in turn encouraging defense contractors to make needed investments in expanded production lines.

Building upon the current list of critical material reserves maintained by DoD’s Defense Logistics Agency (DLA),29 new executive orders and supporting legislation could identify a wider circle of “strategic commodities” for intervention by the federal government to pull demand forward, laying a foundation for broader private sector investment within critical supply chains.30 Depending on the distribution of political capital within a given environment, this line of effort could be initiated at either the congressional or executive level. Ideally, though, DISB reform would employ both approaches in tandem.

The congressional effort would focus on expanding both the definition of “strategic commodities” and increasing stockpiles of these key inputs. One set of levers could feature a newly designated “DLA Strategic Commodities Portfolio” to receive long-term, renewable, guaranteed purchase agreements from the federal government (modeled on the Strategic Petroleum Reserve and primarily administered by DLA31) in order to dramatically expand reserves of these commodities.32 In a slightly different framing, Congress could pass legislation modeled on a “Farm Bill” for designated strategic commodities, which would authorize federal funds for a combination of subsidies and purchase agreements between producers and the government.

To support producers that wish to scale up to meet government targets, Congress could revive a version of the “manufacturing investment companies” (recast, perhaps, as “defense investment companies,” an “industrial finance corporation,” or even a “sovereign wealth fund”) policy concept that was stripped from earlier versions of the chips Act, redesigned to attract institutional investor support.33 This package might also include tax credit and loan guarantee support for base-layer “process gaps” that act as bottlenecks for manufacturers, including software for creating more transparent markets for newly subsidized commodities, enrichment and refining processes, and machine tooling.

Simultaneously, the executive branch could direct the Treasury Department to employ its powers over the Exchange Stabilization Fund (ESF) to guarantee forward demand and therefore dramatically de-risk investment in new projects.34 Deploying a combination of both put option purchases and loan guarantees, the Treasury could effectively lower industry investment hurdle rates (the rate of return firms require to justify greenfield investment) to facilitate production from smaller firms and more speculative projects.35 The president’s DPA Title III authorities could be used complementarily to augment this mechanism.

More speculatively, the breadth of executive power under the Defense Security Cooperation Agency (DSCA), through which the Department of State and Department of Defense jointly administer Foreign Military Sales (FMS) and Foreign Military Financing (FMF) has to date been underexplored. Specifically, it does not seem clear as to whether the executive has the power to issue “war bonds” via these programs, which might not only serve to finance this new policy architecture, but also to increase the real purchasing power of foreign defense budgets, expanding the global market for new U.S. defense exports.

Concurrent with either approach, Congress (via legislation modeled on the Inflation Reduction Act) and the White House (primarily via DPA Title III, and in coordination with state and local governments) could issue a coordinated package of loans, loan guarantees, tax incentives, and subsidies to de-risk investment in new projects aimed at (1) filling new strategic stockpiles and/or (2) responding to Treasury-led signals to stabilize commodities prices.

At the state level, this emergent coalition could lean on state legislatures and promote candidates in favor of enacting permitting reform and deregulation for relevant projects. Modeled on extant state-level policies incentivizing data center and IRA investment, for example, passing state-level legislation to further incentivize investment in commodities production via tax credits and loan guarantees would make an attractive addition to state partisan political platforms, creating a race to the top among state capitals and drawing in additional bipartisan allies at the county and local political levels.

A model DISB bill should account not only for state legislatures, but their executive branches as well. Several state governments, including Republican states ideologically skeptical of state intervention in markets, have robust state economic development agencies. JobsOhio (the semi-privately administered, publicly funded Ohio state development agency) is a powerful example. Proactively designing legislation with these agencies in mind would generate further support at the state government and state donor levels, generating upward pressure on federal delegations to support DISB reform.

A successful DISB reform coalition might, additionally, have interest‑based incentives to pursue a suite of other needed DIB reform proposals, including more efficient co-production arrangements with allies, enhanced competition between both new and incumbent defense contractors, and better federal support for workforce training. More ambitiously, a broad enough coalition may aggregate the political capital to institutionalize DISB reform funding as a renewable government resource in the form of a national bank. This could occur within the initial policy package or, more likely, once the architecture is more mature and has attracted more capital and users. In exchange for the federal government’s underwriting these new revenue streams, current strategic commodities producers and, say, newly formed “strategic commodities investment companies” might agree to divert some percentage of guaranteed government revenues toward capitalizing next-generation production projects within a “National Defense Resource Bank” or, perhaps more realistically, as David McCormick has proposed, a first-loss, capped upside “American Innovation Fund” seeded by the federal government.36

Preemptive Mobilization

This pragmatic approach, if successful, would also generate a coalitional platform for a preemptive arms buildup, ideally to deter any war from occurring in the first place. The fact that America’s reigning corporate coalitions, primarily reliant on protecting intellectual property rather than export-market access, do not have material incentives to press for greater defense spending or military modernization is insufficiently appreciated in Washington.

This represents a significant break from twentieth-century history. The “containment doctrine” that served as the guiding logic of the Marshall and Dodge Plans during the postwar era, for example, would not have been implemented without incentive-based support from both powerful manufacturing interests (intent on securing stable, preferential access to European and Asian import markets) and labor (whose continued bargaining power with capital depended on that market access).37 Similarly, the Reagan defense buildup and neoconservative pivot toward a form of “rollback” could not have been sustained without allies in the financial industry (which, increasingly deregulated, sought greater access to international investment markets) and the ascendent telecommunications and information technology industries (which, also increasingly deregulated, sought access to network effects within international markets).38 Today, however, any logic driving private interest in a forward defense posture has significantly attenuated.

Similar to FDR’s need to generate a new coalition to rearm while the nation remained gridlocked on whether to enter World War II, today’s policymakers must recognize that if they wish to accomplish more ambitious defense goals to prevent (and if necessary, prevail in) a conflict, they must generate an alternative coalition to support it. In the twentieth century, the United States was lucky that the Roosevelt administration had the foresight and, more importantly, the political savvy, to prepare for the worst.

This article originally appeared in American Affairs Volume VIII, Number 4 (Winter 2024): 44–57.

Notes

1 Oz Katerj,

“Fear and Hoarding on Ukraine’s Eastern Front,” Foreign Policy, April 17, 2024.

2 Roxana Tiron and Billy House, “America’s War Machine Can’t Make Basic Artillery Fast Enough,” Bloomberg, June 7, 2024.

3 Sam Skove, “The Goal of 100K Artillery Shells per Month Is Back in Sight, Army Says,” Defense One, April 24, 2024.

4 Tiron and House, “America’s War Machine Can’t Make Basic Artillery Fast Enough.”

5 Office of Local Defense Community Cooperation, Defense Spending by State: Fiscal Year 2022, U.S. Department of Defense, October 2023. To those who would present the natural counterargument to this data, that defense prime and sub-award contracts do not necessarily correspond to where funds are ultimately spent, one might respond that: (a) political power is strongest at the actual nexus between the DoD and vendors written into contracts; and (b) that due to clustering effects, DIB suppliers have historically tended to locate near contract awardees, a trend that has only become more salient with deindustrialization’s advance. For more, see Ann R. Markusen et al., The Rise of the Gunbelt: The Military Remapping of Industrial America, (Oxford: Oxford University Press, 1991).

6 Arthur Herman, Freedom’s Forge: How American Business Produced Victory in World War II (New York: Random House, 2013).

7 Herman M. Schwartz, States versus Markets: Understanding the Global Economy, 4th ed. (London: Bloomsbury Academic, 2022).

8 Dewey W. Grantham, “The South and Congressional Politics,” in Remaking Dixie: The Impact of World War II on the American South, ed. Neil R. Mcmillen (Jackson: University Press of Mississippi, 1997).

9 Paul Krugman, “History and Industry Location: The Case of the Manufacturing Belt,” American Economic Review 81, no. 2 (1991): 80–83.

10 Sam Bocetta, “Abridged History of the Scranton Army Ammunition Plant,” Historical Society of Pennsylvania, September 20, 2017.

11 Markusen et al., Rise of the Gunbelt.

12 John Mintz, “How a Dinner Led to a Feeding Frenzy,” Washington Post, July 4, 1997.

13 Commission on the Future of the United States Aerospace Industry, Final Report of the Commission on the Future of the United States Aerospace Industry, November 2002, 134.

14 Mike Lofgren, “Why Can’t America Build Enough Weapons?,” Washington Monthly, June 23, 2024.

15 Doug Berenson et al., “The U.S. Defense Industry in a New Era,” War on the Rocks, January 13, 2021.

16 Dennis Wille, “The Army and Multi-Domain Operations: Moving beyond AirLand Battle,” New America Foundation, October 1, 2019.

17 Seamus P. Daniels, “What the Fiscal Responsibility Act of 2023 Means for Defense Spending,” Center for Strategic and International Studies, June 15, 2023.

18 Valerine Insinna and Michael Marrow, “SASC Breaks Spending Cap by $25 Billion in FY25 Defense Policy Bill,” Breaking Defense, June 14, 2024.

19 Roger Wicker, 21st Century Peace through Strength: A Generational Investment in the U.S. Military, May 29, 2024.

20 John Costello, Martijn Rasser, and Megan Lamberth, “From Plan to Action: Operationalizing a U.S. National Technology Strategy,” Center for a New American Security, July 29, 2021.

21 Jack Detsch, “The Pentagon Is Trying to Rebuild the Arsenal of Democracy,” Foreign Policy, January 4, 2024. For example, Detsch writes, “Some of the weapons still have to be funded. Congress has already agreed to fund SM-6 and gmlrs. Other projects, such as the Pentagon’s plan to get up to 100,000 rounds of 155 millimeter artillery produced by 2025, need Congress to pass the supplemental budget, LaPlante said. With Congress out for the holidays, that’s on hold until at least January. And across the Atlantic, the European Union has fallen far behind its target of producing 1 million artillery rounds per year to feed Ukraine’s voracious appetite for ammunition while replenishing NATO stockpiles.”

22 Arnab Datta and Alex Turnbull, “IPEF’s OPEC Moment,” American Affairs 7, no. 1 (Spring 2023): 3–16; Arnab Datta and Alex Turnbull, “Contingent Supply: Why Spodumene Reserves May Be the Key to a More Secure Lithium Supply Chain,” Employ America, April 5, 2023.

23 Office of the Under Secretary of Defense for Acquisition and Sustainment, State of Competition Within the Defense Industrial Base, U.S. Department of Defense, February 2022.

24 Department of Defense, “DoD Enters Agreement to Expand Domestic Lithium Mining for U.S. Battery Supply Chains, media release, September 12, 2023.

25 Caterpillar, Inc., “Albemarle and Caterpillar Collaborate to Pioneer Sustainable Mining Technologies and Operations,” media release, September 27, 2023.

26 Albemarle Corporation, “Albemarle and Martin Marietta Sign Innovative Agreement for Beneficial Use of Material from Kings Mountain Mine,” media release, May 8, 2024.

27 Albemarle Corporation, “Albemarle Donates $1 Million to Cleveland Community College to Further Support Workforce Development Programs,” media release, April 17, 2024.

28 Albemarle Corporation, “Permitting Process,” May 2024.

29 For a current list of “Materials of Interest” maintained by the Defense Logistics Agency, see “Defense Logistics Agency Strategic Materials: Materials of Interest,” Defense Logistics Agency, U.S. Department of Defense, accessed October 18, 2024.

30 Defense Logistics Agency, Fact Sheet: Defense Logistics Agency, February 2023; “About: DLA Strategic Materials,” Defense Logistics Agency, accessed October 18, 2024; “An Organizational History of the Defense National Stockpile Center: America’s National Stockpile,” Defense Logistics Agency, accessed October 18, 2024; and for a current list of “Materials of Interest” maintained by DLA, see “Materials of Interest” above.

31 DLA is herein suggested as the primary administrator of the stockpiles given its extant legal authority and technical capacity for doing so. However, given the necessity for political compromise at the bureaucratic level to broaden support, splitting administration of these stockpiles, i.e., between the Departments of Defense, Energy, and Commerce, might be necessary.

32 Defense Logistics Agency, Fact Sheet; “About: DLA Strategic Materials,” Defense Logistics Agency; and Clifton Chappell et al., An Organizational History of the Defense National Stockpile Center: America’s National Stockpile, Defense Logistics Agency, accessed October 18, 2024.

33 Lee Harris, “Commerce Department Could Pay Manufacturers to Reshore Critical Production,” American Prospect, May 25, 2022.

34 Alex Williams, Arnab Datta, and Skanda Amarnath, “The Biden Administration Has the Power: Administrative Authority to Address the Crisis in Oil Supply Right Now,” Employ America, March 9, 2022.

35 Julius Krein, “Steering Finance,” Boston Review, September 15, 2021.

36 David McCormick, Superpower in Peril: A Battle Plan to Renew America (New York: Center Street, 2023).

37 Gary Gerstle, The Rise and Fall of the Neoliberal Order: America and the World in the Free Market Era (New York: Oxford University Press, 2022); Herman M. Schwartz, States versus Markets.

38 Gerstle, Rise and Fall of the Neoliberal Order.